Good morning

There are only a few data points to watch today such as the Eurozone labour costs for the first quarter or consumer confidence for May. As the June ECB meeting draws closer the number of ECB speakers appears to be picking up with Wunsch, Knot and Cipollone scheduled for today. The US speakers schedule is also busier for the day as we will hear from Bostic, Barkin, Collins and Musalem.

Moody’s downgrade has turned the spotlight back on US fiscal dynamics and the question whether there is any serious intent by politicians to rein in the deficit. The US has now lost its last AAA rating, although it was not really a surprise. S&P had downgraded the US from its highest level already in 2011. Back then, however, the market reaction was quite different – the reaction was a flight to safety which ultimately benefited Treasuries. US rates remain under pressure with 10-Y yields testing beyond the 4.5% level again.

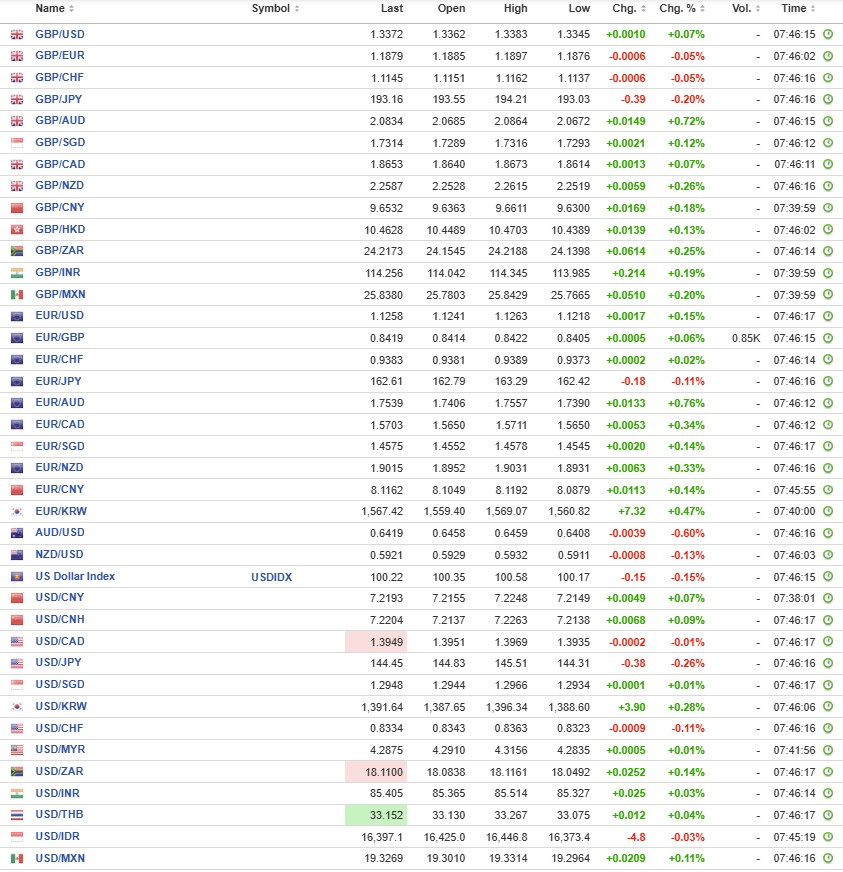

De-dollarisation continues to gain traction, with synchronised selling of USD, Treasuries, and US equities signaling a broader erosion of confidence in US assets. The market appears keen to resume the "Sell America" trade whenever the opportunity arises. The USD index steadied overnight to 100.22, close to a one-week low.

Meanwhile, Fed’s Williams has said that policy uncertainty has led to the Fed keeping policy rate on hold. There’s a lack of clarity in the path forward for monetary policy over the coming months. He thinks a rate cut in June is unlikely, while the Fed will remain data dependent when determining the next policy move. The US leading index fell 1%m/m in April, worsening from a 0.8% drop in March. A potential slowdown in the US economy in H2 due to higher tariffs could lead the Fed to ease policy.

In geopolitics, following Trump's call with Putin, Trump stated that Russia and Ukraine would commence immediate negotiations aimed at achieving a ceasefire and ending the war, though the Kremlin cautioned the process would require time. Trump briefed Zelensky and EU leaders in a group call. European leaders agreed to intensify sanctions on Russia, while Trump opted not to introduce fresh sanctions.

The Euro has outperformed its G10 peers in recent sessions, EUR/USD remains steady around 1.1240 supported also by ECB President Lagarde’s comments framing recent Euro strength as a reflection of a shift in global capital away from the US dollar and fading confidence in US economic policies.

The head of the Swiss National Bank (SNB), Martin Schlegel, said that inflation in the country can turn negative in certain months this year. In this respect, the central bank, according to Schlegel, is prepared to bring the interest rate into negative territory if required. Interest rates remain the main policy tool of the SNB, but FX interventions might also be put in place. Markets expected SNB to cut the policy rate from 0.25% to 0.0% in June. EUR/CHF, after a CHF rally early April, recently held a tight range between 0.93 and 0.945.

Sterling hovers north of EUR/GBP 0.84. Yesterday’s announcement of a broad-ranging post-Brexit deal where defence lies at the centre had limited impact. The UK releases CPI numbers tomorrow.

USD/JPY returned sub 145 with JPY extending gains this morning after Japan’s finance minister Kato is arranging a meeting with US Treasury Secretary Bessent to discuss FX.

The RBA cut interest rates by 25bp to 3.85% as expected but the central bank remained uncommitted towards future easing, maintaining its data-driven stance towards future easing. The RBA cut its 2025 GDP forecast to 2.1% highlighting increasing risks to the economy from global trade uncertainty. AUD/USD eased to $0.6423 down from $0.6459 following the announcement.

China retail sales grew 5.1%y/y in April, down from +5.9%y/y in March and missing Bloomberg estimates of 5.8%y/y growth. The PBoC reduced its benchmark lending rates for the first time since October 2024, aiming to bolster economic growth amid ongoing trade tensions with the U.S. The one-year loan prime rate (LPR) was lowered by 10bp to 3.0%, and the five-year LPR, a key reference for mortgage rates, was cut to 3.5% from 3.6%. The rate cuts aim to stimulate consumption and loan growth as the economy softens. However, the Chinese yuan’s offshore pair USD/CNH and onshore pair USD/CNY were both steady at 7.2203 and 7.2198.

Other regional currencies were largely unchanged with USD/KRW the outlier with the pair up 0.5% overnight to 1,391.24.

| Interest Rate Swaps | EUR | USD | GBP |

| 3Y | 2.08 | 3.68 | 3.80 |

| 5Y | 2.24 | 3.70 | 3.85 |

| 10Y | 2.54 | 3.91 | 4.14 |