just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

The week the market stopped paying any price for a perfect story.

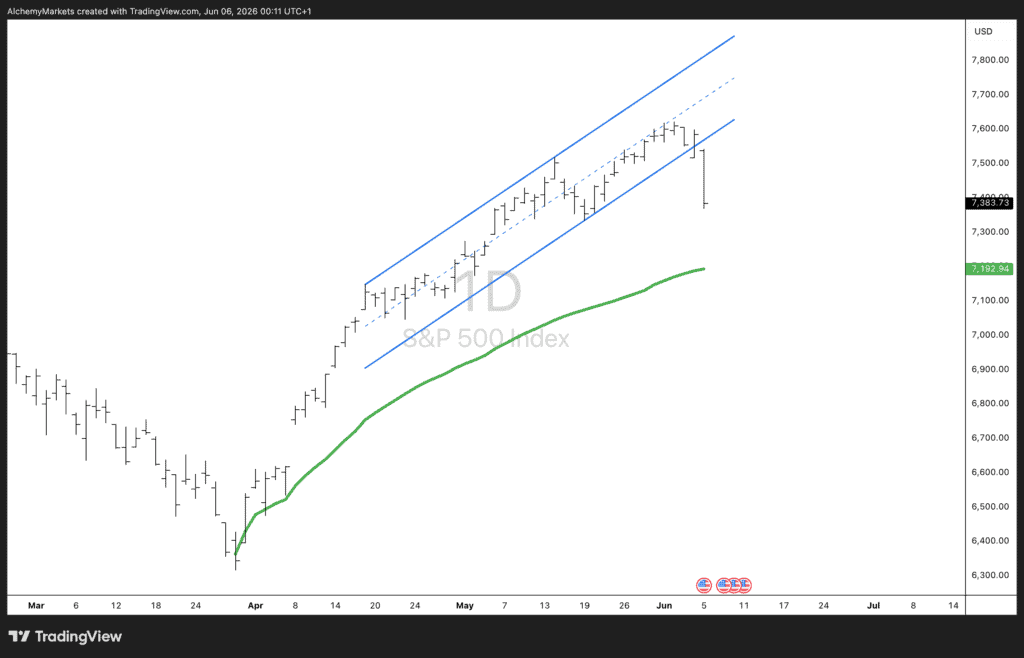

For the better part of a year, the S&P 500 has run on a single engine: artificial intelligence, and the belief that the spending behind it has no ceiling. Every quarter the numbers got bigger, every dip got bought, and the index climbed a clean channel from the April low near 6,300 all the way to a record print above 7,600. Then, in the space of 48 hours, the market was handed two of the things it had been quietly counting on — and sold them both.

That is the story worth telling this week. Not that stocks fell, but why they fell, and what it says about the year ahead.

The first crack came from Broadcom. On the surface the quarter was a triumph: second-quarter revenue of $22.19 billion, up 48% from a year earlier, with AI chip sales reaching $10.8 billion, a 143% increase. By any normal standard, that is a blowout. And yet the stock fell roughly 14% in after-hours trading. The reason is the tell. Management guided next-quarter AI chip sales to about $16 billion versus the roughly $17.2 billion some analysts expected, and crucially kept its full-year AI target unchanged rather than raising it. The number was extraordinary. The problem was that the market had already priced more than extraordinary. When the full-year math landed at $56 billion rather than higher, traders read it as a ceiling rather than a floor.

The second crack came from the labour market — but in reverse. On Friday, nonfarm payrolls jumped a seasonally adjusted 172,000 in May, far above the consensus estimate for 80,000, with the unemployment rate holding at 4.3%. A strong economy should be good news. The catch is what it does to the Fed. A labour market this resilient reduces the urgency for near-term rate cuts, suggesting a prolonged period of stable rates — and high-valuation stocks faced downward pressure as a result. Good news for Main Street, bad news for a market that had been leaning on cheaper money to justify rich multiples.

Put them together and you get the real theme: the market is no longer being rewarded for good. It needs perfect, and it needs it cheap. Broadcom proved that even a 143% growth print can disappoint when expectations run ahead of reality. The jobs report proved that the rate-cut cushion stocks were resting on is thinner than hoped. Two different sources, one message — the margin for error has gone.

Step back and this looks less like a single bad week and more like the first real test of the move off the April low. The entire rally from 6,300 has been a story of expanding belief: belief that AI capex compounds forever, belief that the Fed rides to the rescue at the first sign of trouble, belief that any pullback is a dip to be bought. Channels like the one SPX has traced don't break because the story turns false — they break when the story stops getting better. Broadcom's "unchanged" guidance and Friday's "too strong" payrolls are both, in their own way, the story failing to improve.

That doesn't make this a top. The bull case is still intact — AI bookings are contracted, not hoped for, and a resilient economy is a strange thing to be bearish about. But the easy phase, where price simply tracked the upper rail and nobody had to think, looks finished. From here the index has to earn its level rather than assume it. The question for the back half of 2026 is no longer "how high," it's "what price is fair" — and that is a far more two-sided conversation.

Price has just slipped out of the lower boundary of the rising channel that has guided the entire move since April, closing the week around 7,383. That break is the technical echo of the fundamental shift above — the trend isn't broken, but it's no longer effortless.

The level to watch is 7,400. It was support on the way up; it now sits just overhead as the first test of whether buyers step back in or sellers defend the breakdown. A clean rejection below 7,400 opens the door toward the anchored VWAP from the April low (the green line), which has tracked beneath this entire advance and currently sits near 7,200. That is the line the rally has never seriously challenged — and the most logical magnet if this turns into a genuine mean-reversion rather than a one-week wobble. Reclaim 7,400 convincingly and the breakdown reads as a shakeout; lose it and the VWAP becomes the conversation.

Chart: S&P 500 Index, Daily timeframe. Rising channel off the April low, anchored VWAP in green.

After the Broadcom-and-payrolls double-header, the calendar front-loads the quiet and back-loads the fireworks. Monday and Tuesday are bare. Then everything lands at once.

| DayEventWhy it matters | ||

| Mon 9 Jun | — | No major scheduled releases. |

| Tue 10 Jun | — | No major scheduled releases. |

| Wed 11 Jun | US CPI | The headline US event. After a hot payrolls print, a firm CPI would cement the "no cuts soon" read and pressure rate-sensitive growth names further. |

| Wed 11 Jun | China CPI | Read on global demand and the commodity complex; matters for risk appetite broadly. |

| Wed 11 Jun | Bank of Canada decision | A second G7 central-bank data point in the same week. |

| Thu 12 Jun | ECB rate decision + staff projections | Markets price ~91% odds of a 25bp hike to 2.25%. The projections and Lagarde's tone are the real catalyst, not the near-certain hike. |

| Thu 12 Jun | US PPI | Pipeline inflation read; confirms or complicates the CPI signal. |

| Fri 13 Jun | German final CPI | Confirms the euro-area inflation picture into the ECB. |

| Fri 13 Jun | UoM Consumer Sentiment (prelim) | Closes the week on the US consumer's mood and inflation expectations. |

The thread that ties it together: Wednesday's CPI is now the single most important release for US equities. Friday's jobs report told the Fed it can wait; a hot CPI would tell it it must wait. For an S&P 500 that just lost its channel on exactly that fear, the inflation print is the data that either rescues the dip or confirms the breakdown.

Alchemy Markets is a multi-asset brokerage providing retail traders with the same elite trading conditions, tools, and transparency typically reserved for institutions.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.