Good morning

The IMF has downgraded its global growth forecast by 0.5ppt to 2.8% in 2025, from 3.3% previously. This would mark the slowest pace of expansion since the Covid pandemic in 2020. It has also cut its world growth outlook for 2026 by 0.3ppt to 3%, while warning the risks to global growth remain to the downside. Notably, IMF has revised down US GDP growth to 1.8% in 2025 and 1.7% in 2026, from 2.7% and 2.1% respectively, while China’s GDP growth is now seen at 4% in 2025 and 2026, down from 4.6% and 4.5% in previous projections.

The rally in gold has been underpinned by President Trump’s trade war 2.0, along with his earlier threat of firing Fed Chair Powell, which has driven demand for haven assets. Japan Prime Minister will look to discuss currencies with US Treasury Secretary Scott Bessent this week. And despite trade uncertainties, the BOJ sees little need to adjust its stance of gradual policy rate hike for now, while seeing the risk that trade war 2.0 could weaken the Japanese economy and slow the progress towards the bank’s target of sustainable inflation at 2%.

The rally in gold has been underpinned by President Trump’s trade war 2.0, along with his earlier threat of firing Fed Chair Powell, which has driven demand for haven assets. Japan Prime Minister will look to discuss currencies with US Treasury Secretary Scott Bessent this week. And despite trade uncertainties, the BOJ sees little need to adjust its stance of gradual policy rate hike for now, while seeing the risk that trade war 2.0 could weaken the Japanese economy and slow the progress towards the bank’s target of sustainable inflation at 2%.

Meanwhile, Trump has reportedly said that he is open to negotiating with China and hinted at partial reduction of tariffs on China if a deal is made. Both sides are reportedly set to hold talks in early May. He has also reportedly said that he has no intention of firing Fed Chair Powell. It remains to be seen if Trump will flip again in his next set of comments or social media tweets.

For today the April PMIs for France and Germany are all expected to come in weaker, but the Eurozone aggregate PMI is still expected to remain just above 50. Consensus sees a moderate weakening of the US PMIs, with the composite index coming down from 53.5 to 52.2. From the ECB there are also the wage tracker readings, but with focus back to growth concerns, these numbers may not get much attention. Other data from the US includes the Fed’s Beige Book, which could give insights into possible price hikes by businesses in reaction to tariffs.

Meanwhile, Trump has reportedly said that he is open to negotiating with China and hinted at partial reduction of tariffs on China if a deal is made. Both sides are reportedly set to hold talks in early May. He has also reportedly said that he has no intention of firing Fed Chair Powell. It remains to be seen if Trump will flip again in his next set of comments or social media tweets.

For today the April PMIs for France and Germany are all expected to come in weaker, but the Eurozone aggregate PMI is still expected to remain just above 50. Consensus sees a moderate weakening of the US PMIs, with the composite index coming down from 53.5 to 52.2. From the ECB there are also the wage tracker readings, but with focus back to growth concerns, these numbers may not get much attention. Other data from the US includes the Fed’s Beige Book, which could give insights into possible price hikes by businesses in reaction to tariffs.

Plenty of prominent central bankers are scheduled for speeches and discussions in Washington at the Institute of International Finance. Chief economist Lane from the ECB will speak, as will Knot and Villeroy. From the Fed we have Goolsbee, Musalem, Hammack and Waller. Bailey and Breeden from the Bank of England will speak.

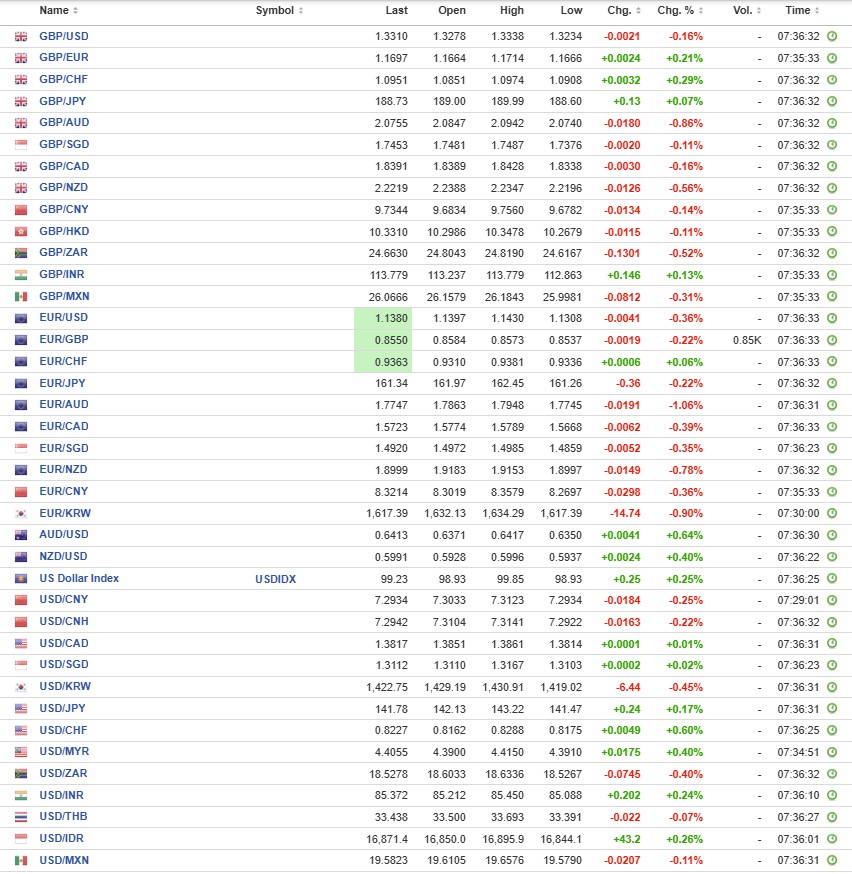

The USD Index rose 0.3% to 99.22 after regaining some ground from a three-year low on Tuesday.

EUR/USD edged lower toward the 1.14 mark, as the broader USD staged a modest rebound across the G10 space. Overall, with investor confidence in US assets continuing to deteriorate and concerns over the economic outlook potentially deepening, traders continue to buy EUR/USD on dips and still maintain a strategically bullish stance on the cross. That said, EUR/USD remains almost entirely a function of US moves.

GBP/USD extended its losses overnight trading around 1.3300 after pulling back from a 7-month high of $1.3424. The pound will look at today’s PMIs to gauge the drop in business sentiment due to US tariffs. Similar to the Eurozone, the expected decline in the composite PMIs is unlikely to be enough to take the index below the 50.0 level. Unlike the ECB, these surveys are not particularly regarded by the Bank of England, which remains fundamentally more concerned about inflation.

USD/JPY edged 0.3% higher in Asian trade to around 141.85 after two days of sharp declines. Data showed that Japanese manufacturing activity shrank for the tenth consecutive month in April as new orders declined significantly amid U.S. tariff concerns. The au Jibun Bank manufacturing PMI came in at 48.5 in April, below the forecast of 48.7. Meanwhile, Japanese services activity rebounded, with the au Jibun Bank services PMI rising to 52.2 in April, from a neutral reading of 50.0 in March. The overall composite PMI expanded to 51.1 in April from 48.9 in March.

| Interest Rate Swaps | EUR | USD | GBP |

| 3Y | 1.95 | 3.51 | 3.63 |

| 5Y | 2.13 | 3.60 | 3.70 |

| 10Y | 2.46 | 3.85 | 4.05 |