Good morning

Markets have reduced some tariff related risk premia for now, with the US 10-year yield falling back to nearly the pre-US election level at 4.27%, from a mid-January peak of 4.80%. The US dollar index has also fallen to the 106.30-level after peaking at 110.00. But the latest news is that Trump will not be stopping tariffs. He has said that “tariffs will go on, not all but a lot of them”. He has also announced that the 25% delayed tariffs on Canada and Mexico will come into effect on 2 April, while he plans to impose tariffs on EU, with 25% on autos, among other things. GBP, USD and JPY all made gains yesterday, while Scandies, AUD, and NZD came under some selling pressure on a day where risk sentiment overall was mixed.

Nvidia earnings were strong, but didn’t trigger a strong directional move in the company’s share price afterwards and don’t set the tone for trading this morning. Today’s eco calendar contains Minutes of the previous ECB meeting along with Spanish CPI and US durable goods orders, but risk sentiment will remain the key market driver. Attention is already turning to tomorrow's German and French CPI prints, alongside the US PCE release. The PCE price index, the Fed's preferred inflation gauge, will provide critical information on consumer spending and price trends, especially at time the central bank has maintained its hawkish stance citing sticky inflation.

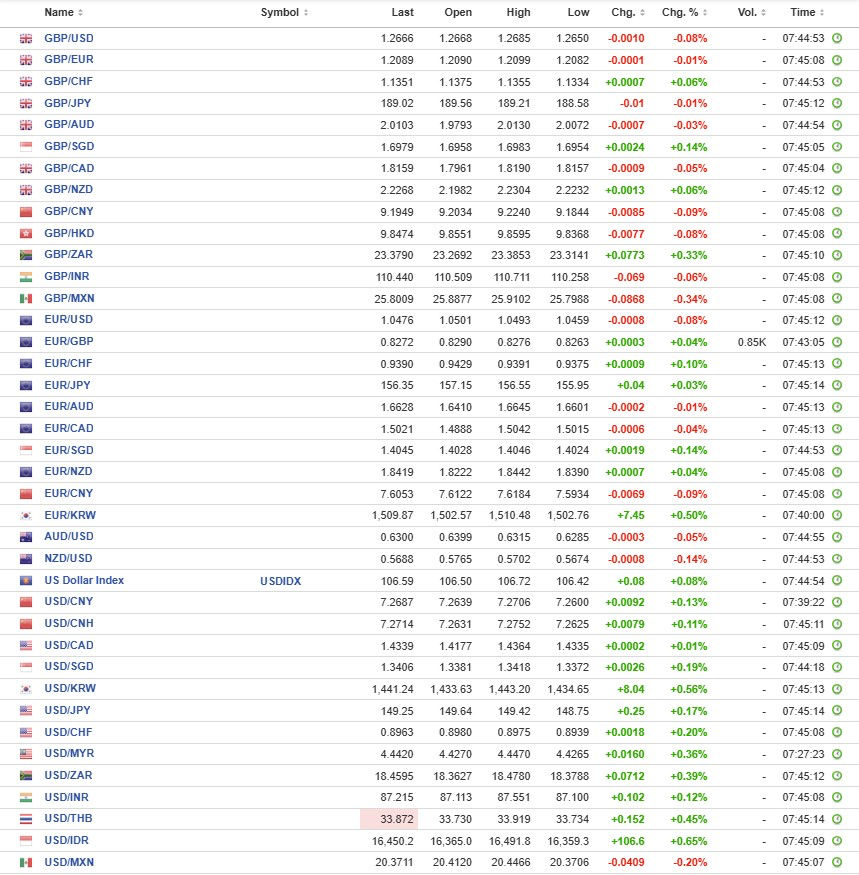

Traders continue to expect EUR/USD to trade within a tight range around 1.05 in the near term. However, if softer US data momentum persists, risks remain skewed toward some tactical upside. EUR/USD opens the European session on the defensive around 1.0465.

EUR/GBP extends its losses for the second consecutive day, trading around 0.8270. Meanwhile, BoE’s MPC Member Swati Dhingra highlighted the limitations of central bank policy in addressing trade-based supply shocks. Dhingra noted that if global economic fragmentation proceeds in an orderly fashion, monetary policy interventions may not be necessary. However, in a scenario where external supply shocks become more frequent, having an independent monetary authority with a clear inflation target becomes crucial.

USD/JPY is trading near YTD lows around the 149 level. Narrowing rate differentials between Japan and G10 economies have been the primary driver of JPY outperformance this year. The 2-Y yield differential between Japan and the US has tightened to around 3.3pp - the lowest since October - suggesting further downside potential for USD/JPY. With G10 FX generally lacking direction amid policy uncertainty, the JPY's safe-haven appeal, alongside declining oil prices, likely also plays a role. The key risk of another leg lower in USD/JPY is that long JPY has increasingly become a consensus trade, with recent IMM positioning data indicating stretched long JPY positions.

The Chinese yuan’s offshore pair USD/CNH gained 0.3% to 7.2746, while the onshore pair USD/CNY was up 0.1% at 7.2705.

China plans to recapitalise three of its largest banks over the coming months, namely Agricultural Bank of China Ltd., Bank of Communications Co., and Postal Savings Bank of China Co. via injecting at least RMB400 billion ($55bn) of fresh capital. This is an initial move that seek to strengthen the banking sector, despite the six largest local banks having adequate capital that exceed requirements.

The Indonesian rupiah’s USD/IDR pair, and the South Korean won’s USD/KRW climbed 0.6%, each to 16,435.5 and 1,441.02, leading losses among regional currencies. The Indian rupee’s USD/INR pair advanced 0.3% to around 87.251. Continuing capital outflows are weighing on the Indian rupee, but RBI intervention will likely cap the downside for now.

The Bank of Thailand cut its policy rate by 25bp to 2.00% this month, given weaker than expected CPI inflation and economic recovery. BoT assesses that this rate adjustment is consistent with current economic conditions and remains robust to economic risks going forward. In terms of the USD/THB outlook, consensus is for the pair to rise to 35.30-level in Q1 and 36.00 in Q2.

| Interest Rate Swaps | EUR | USD | GBP |

| 3Y | 2.19 | 3.83 | 3.98 |

| 5Y | 2.23 | 3.80 | 3.93 |

| 10Y | 2.36 | 3.84 | 4.01 |