Good morning

The ECB meeting will be the main focus in the Eurozone and thus the retail sales numbers from January will likely draw little attention. The ECB is still widely expected to cut the deposit facility rate by 25bp to 2.5% later today. The market has repriced its expectations, with a cut at the April meeting already only a coin toss and overall the ECB looks likely to end the cycle at 2%.

From the US we have trade balance numbers and wholesale inventories, but given these numbers are from January they may not yet offer insights into the impact from Trump’s policies. Jobless claims, on the other hand, could be watched more closely since these are from March and therefore give a timelier feel of recent job market developments. Lastly, the Fed’s Waller will speak about the economic outlook. The US administration is walking a tightrope between getting what it wants through tariffs and the negative boomerang effect on the US economy.

Rarely if ever have European yields spiked by 30bp while US Treasuries idle. The market moves in Europe reflect a fundamental repricing of the Eurozone outlook and are not just about increased Bund issuance. The 10Y Bund yield now stands at 2.8%, the highest level since 2023, and this was when inflation just came down from double-digit numbers. The narrative of US strength versus European malaise is now being seriously questioned by the markets. The ECB will likely give little forward guidance but may lighten the language on rates being restrictive.

The US economic data released yesterday was mixed, though. ADP employment rose 77k in February, slower than the 183k increase in January, missing Bloomberg consensus of 140k. But the ISM services index was stronger than expected, rising to 53.5 in February, from 52.8 in January. Both new orders and employment also expanded, though the services prices paid sub-index jumped to 62.6 from 60.4 in January. Markets have continued to price in about 3 rate cuts for the rest of this year, while the US dollar index has fallen by 2.6% this week to currently trade around 104.22.

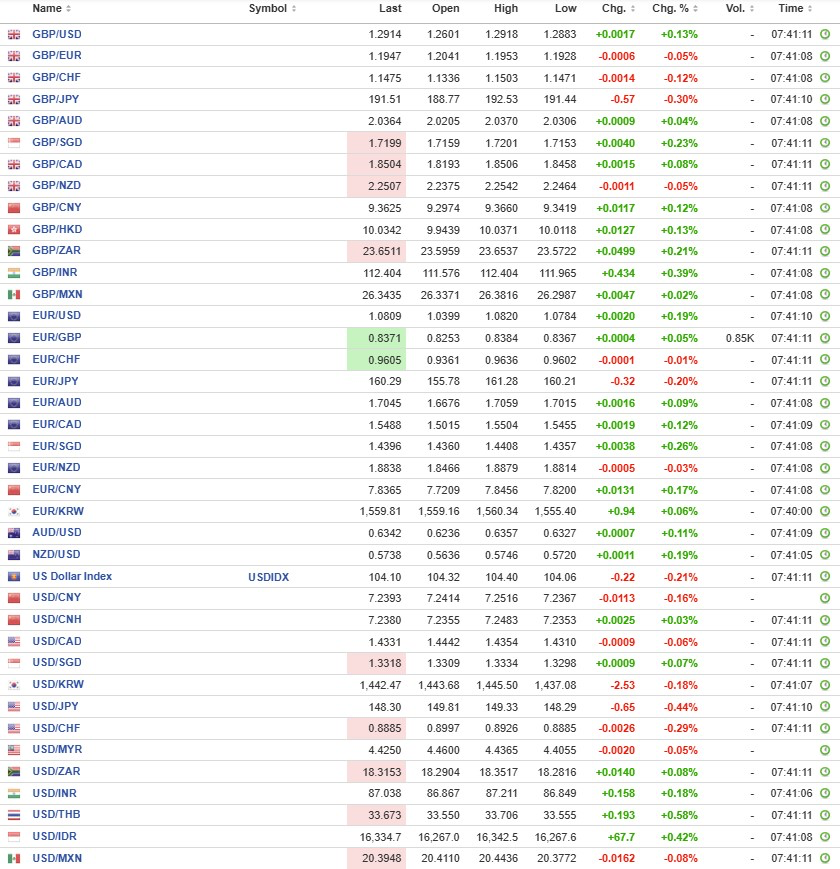

Meanwhile, EUR/USD started the week at 1.0372 and closed yesterday at 1.0789, on the back of Germany’s proposed plans to exempt defence and security spending from limiting fiscal spending and to set up a EUR500bln infrastructure plan.

EUR/GBP moved higher on the back of broad-based EUR optimism and combined with the high-volatility environment, which weighed on GBP. The UK’s Institute for Fiscal Studies, a leading think tank, said chancellor Reeves may soon have to choose which promise she’ll have to break and either raise taxes or return to austerity. The UK presents an update to the budget in its spring forecast on March 26.

CHF was among the big losers yesterday with EUR/CHF rising 1.5% during yesterday's session. While Swiss inflation surprised slightly to the topside, this failed to support the Swiss Franc. The SNB still looks on track to cut rates at the next meeting on March 20.

In Japan, BoJ Deputy Governor Uchida has signaled that the bank remains on a rate normalisation path, while adding that it’s unlikely for the bank to do back-to-back rate hikes while the policy rate will eventually rise to at least 1% by end of FY2026. This could continue to put modest downward pressure on USD/JPY which has opened the European session around 148.83.

Momentum and FX positioning data point to USD declines for now, with Asian currencies further strengthening against the USD amid improving risk appetite.

USD/CNY eased 0.1% to 7.2417 following a substantially stronger-than-expected midpoint fix from the PBOC. Sentiment towards China was also lifted by Beijing highlighting plans for higher fiscal spending this year, aimed chiefly at shoring up weak consumption and supporting economic growth.

| Interest Rate Swaps | EUR | USD | GBP |

| 3Y | 2.39 | 3.80 | 4.07 |

| 5Y | 2.49 | 3.79 | 4.05 |

| 10Y | 2.64 | 3.86 | 4.15 |