Good morning

Ahead Today G3: Speeches by Fed’s Collins and Harker, Germany’s industrial production to tolerate a weaker CNY to help offset

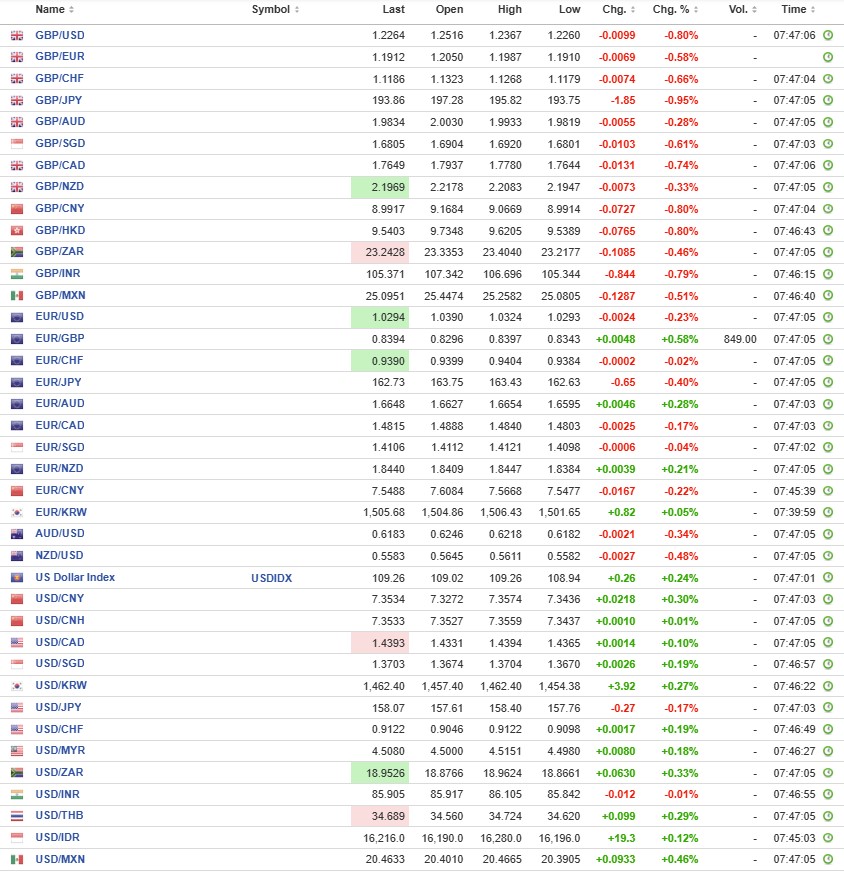

The broad US dollar index (DXY) gained by 0.5% in Wednesday’s session, amid persisting “Trump trades” and several recent stronger than expected US economic data. Several G10 currencies fell against the US dollar, more notably GBP (+1%). USD/JPY has also risen above the 158.00 level. Donald Trump has reportedly considered declaring a national economic emergency to impose tariffs on trading partners. During his presidential campaign, he pledged to impose 60% tariffs on imports from China and 10% on imports from everyone else. Meanwhile, US initial jobless claims fell to 201k in the week ending 4 January, from 211k in the prior week, keeping historically low.

Meanwhile, Fed’s Waller has said inflation will continue to decline towards the Fed’s 2% target, supporting more rate cuts this year. However, he added that the pace of rate cuts will still depend on inflation progress. He also mentioned that tariffs are not likely to have a persistent effect on inflation, and thus potential tariff hikes will not affect his view of more policy easing.

The focus in the US today will be speeches from the Fed’s Collins and Harker as well as Challenger jobs data. US stock markets are closed and its bond markets leave early due to a national day of mourning for ex-president Carter. From Germany we will receive industrial production numbers for November, which are expected to have risen by 0.5%y/y. For the Eurozone as a whole we have retail numbers.

The USD index steadied in Asian trade to 109.12 but remains on the front-foot. The minutes of the Fed’s December meeting showed policymakers growing increasingly geared towards a slower pace of rate cuts in 2025. Fed members also expressed some concerns over expansionary policies under President-elect Donald Trump potentially underpinning inflation.

v

UK gilts and sterling suffered steep losses yesterday as traders took aim at UK assets. Yields soared another 4.5-11.3bp. The 10-yr yield (+11.3bp to 4.79%) surpassed the previous post-pandemic highs to hit the highest levels since ’08. The 30-yr yield already smashed Tuesday’s 27-yr high by adding another 10.9bp to 5.35%. Such underperformance at the long end of the curve reveals fiscal and inflation risks are the driving force. EUR/GBP shot up from 0.828 towards 0.835 and is extending gains in European trading this morning. GBP/USD also under pressure with the pair testing April 2024 support at 1.23.

EUR/CHF tracked higher during yesterday's session amid a soft twist to the December Swiss inflation print. Swiss inflation for December came in broadly in line with expectations, meeting the SNB's Q4 2024 forecast of 0.7%y/y. Headline came in at 0.6%y/y (cons: 0.6%, prior: 0.7%) and core at 0.7%y/y (cons: 0.8%, prior: 0.9%). The SNB remains on track for delivering another cut in March, there are another two inflation prints before the next meeting on 20 March. Traders stay positive on the CHF on narrowing rate differentials to the ECB and fundamentals. As recent data has indicated, the SNB remains side-lined on FX intervention.

USD/JPY eased 0.3% back below 158 yen following stronger than expected Japanese wage data that will continue to underpin inflation and give the BoJ more impetus to hike rates sooner rather than later. Traders suggest the case was building for a January hike, although it would still be a close call.

AUD/USD fell 0.1% to $0.6196 as data showed retail sales grew less than expected in November, despite support from the Black Friday shopping event. But Australia’s trade balance grew more than expected in November, on support from strong commodity exports.

USD/CNY has been hovering near the upper bound of its trading band in recent days above the key 7.3 level. PBOC has continued to set its daily fixing rate for USD/CNY below the 7.2000 level to slow the pace of CNY depreciation. However, it may be inevitable for the PBOC to tolerate a weaker CNY to help offset the negative impact of potential higher US tariffs. China December inflation data published this morning showed that deflationary tendencies remain in place despite multiple government efforts to revive domestic demand. CPI inflation was unchanged in November (0.0% m/m), lowering the y/y measure from 0.2% to 0.1%. At 1.61%, China’s 10-yr government bond yields stabilises near record low levels.

USD/KRW eased marginally to 1,461.03, amid continued efforts to arrest President Yoon Suk Yeol over a failed attempt to impose military law. USD/SGD pair was steady trading around 1.3700, while the Indian rupee’s USD/INR pair hovered just below the 86 rupee level.