just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

This week’s CPI report came in modestly softer than expected. Headline inflation printed 0.2% month-over-month versus 0.3% expected, while year-over-year slowed to 2.4%. Core inflation held at 0.3% MoM and 2.5% YoY.

At first glance, the market response made sense. Yields softened, duration assets caught a bid, and equities pushed higher. The narrative was straightforward: inflation is easing, rate-cut probabilities tick higher, and financial conditions loosen slightly.

But that interpretation only captures the first-order effect.

Core inflation at 0.3% monthly still annualizes to roughly 3.6%. That is not consistent with a clean return to target. This was not a regime shift in inflation dynamics — it was incremental cooling within a still-sticky core trend.

What this CPI print accomplished was subtle:

What it did not do was materially alter forward earnings expectations.

That distinction matters. Liquidity can fuel tactical extensions. Sustainable rallies require earnings reinforcement.

The post-CPI move appears more positioning-driven than fundamentally driven. If the market leaned cautious into the print, a softer read forces mechanical adjustment: duration short covering, systematic fund re-leveraging, and incremental equity exposure.

But beyond positioning, the more important question is whether this data changes the earnings trajectory.

Does slightly cooler inflation:

The answer, at least for now, is that the effects are marginal rather than transformative.

This keeps the rally dependent on liquidity dynamics rather than upward revisions in growth expectations. And rallies driven primarily by liquidity tend to weaken over successive impulses unless fundamentals re-accelerate.

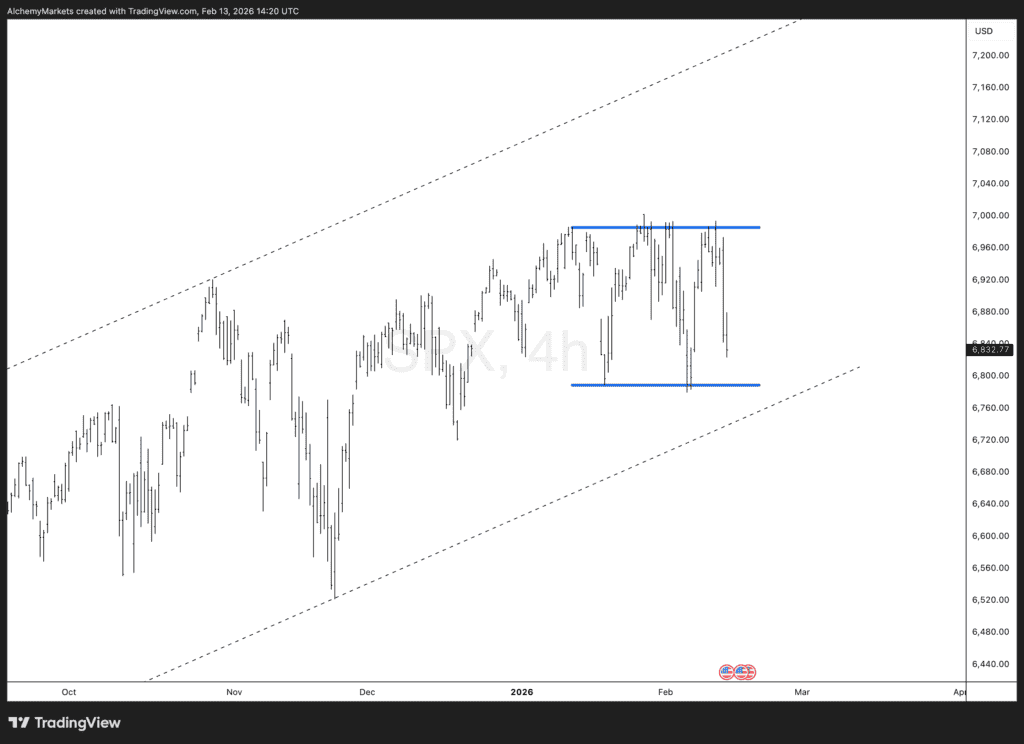

The SPX remains in a constructive technical posture, but price action has shifted from expansion to compression.

The index is consolidating near range highs within a broader rising channel. Higher lows remain intact, but upside progress has slowed as resistance caps immediate momentum. Volatility has compressed and momentum indicators have cooled — classic characteristics of digestion rather than distribution.

This is not bearish structure. It is a pause.

Markets tend to move in sequences: impulse, consolidation, impulse. We are currently in the consolidation phase. A decisive breakout above range resistance would likely trigger another leg higher as systematic flows and momentum strategies re-engage.

However, the durability of that next impulse is the real issue.

Each successive breakout has required expanding liquidity, improving breadth, and stable or rising earnings expectations. At present:

That means the market may well produce another upside break. But the internal strength behind it will be scrutinized more closely than prior legs.

The question is no longer whether SPX can make new highs. It is whether the market has enough internal momentum for another sustained expansion, or whether upside velocity begins to fade without fresh macro or earnings catalysts.

Sideways action near highs is healthy. But repeated breakouts without reinforcement eventually lose torque.

Three events stand out as relevant to this framework.

Building permits offer forward-looking insight into housing and construction activity. With inflation cooling slightly, this release will help determine whether demand is stabilizing or softening.

If permits strengthen, it supports the interpretation that CPI cooling reflects supply normalization rather than demand erosion. That would reinforce the soft-landing narrative and support rate-sensitive segments of the market.

If permits weaken, the inflation moderation could instead be interpreted as slowing demand. That would increase the risk that earnings expectations face pressure in coming weeks.

Housing is one of the clearest transmission channels from rates into the real economy. This data point carries more signal than the headline often suggests.

The Reserve Bank of New Zealand decision will not directly drive U.S. equities, but it does contribute to the global liquidity backdrop.

A dovish tone would reinforce global easing expectations and potentially keep downward pressure on global yields. A hawkish stance, by contrast, could temper enthusiasm around the timing and breadth of global rate cuts.

In a market sensitive to policy trajectory, even incremental shifts in global central bank tone can influence risk appetite.

Consumer sentiment closes the week and may prove decisive in shaping positioning.

Confidence is a proxy for future spending behavior. Strong sentiment would reinforce the soft-landing narrative and support discretionary demand assumptions. Weak sentiment, especially alongside cooling inflation, risks shifting the narrative toward demand deceleration.

That distinction is critical. Inflation cooling due to supply improvement is constructive. Inflation cooling due to weakening demand carries very different earnings implications.

The CPI report modestly reduced inflation risk but did not signal structural disinflation. SPX remains technically constructive but range-bound. The setup allows for another breakout attempt, particularly if housing and sentiment data confirm economic resilience.

However, sustainability will depend on whether:

Liquidity can power the next move. But without reinforcement from growth and revisions, each successive impulse becomes harder to extend.

The market may attempt another leg higher.

The real debate is whether it still has the internal strength to sustain it.

Alchemy Markets is a multi-asset brokerage providing retail traders with the same elite trading conditions, tools, and transparency typically reserved for institutions.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.