just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

Each year, the world’s most powerful central bankers and economists gather in the remote peaks of Jackson Hole, Wyoming. But while the setting is serene, the implications are seismic.

This year's symposium, titled “Labour Markets in Transition”, is poised to be a policy-defining moment for Fed Chair Jerome Powell—and for markets hungry for clarity on inflation, interest rates, and the future of monetary policy.

With inflation cooling modestly and growth showing signs of fatigue, investors are betting on at least one rate cut by September. But the Fed’s language has stayed cautious. And with internal politics heating up—amid debates over independence, presidential influence, and even succession—the stakes for Powell’s Jackson Hole address couldn’t be higher.

Tariffs, particularly those targeting Chinese electric vehicles and semiconductors, are once again inflating input costs. July import prices rose 0.4%, the first solid jump in months. But who’s eating that cost?

Data suggests U.S. corporations are still absorbing the blow, lacking pricing power to pass it on. This deflationary absorption may buy Powell time. However, with retail inventories declining—especially in autos—companies may soon be forced to hike prices.

Powell will likely acknowledge that inflation risks remain skewed to the upside. But whether they’re persistent enough to delay a rate cut remains to be seen.

In July, Powell said the labour market wasn’t weakening. Two days later, a shock revision to payrolls painted a different picture. Job growth slowed, and confidence surveys like ISM and U. of Michigan echo labour weakness.

While Powell may downplay payroll revisions in favour of the unemployment rate (still below 4%), sluggish wage growth contradicts the idea of a tight labour supply.

With the symposium themed around labour, expect Powell to walk a fine line: acknowledging softness without triggering panic.

Markets are fully pricing in a September cut. But Powell might hesitate to pre-commit. Why? One more jobs and inflation print is due before the September meeting.

Expect Powell to re-emphasise data dependence, possibly tempering expectations. But he’s unlikely to strongly oppose a market already banking on easing—unless the next data sets surprise to the upside.

Treasury Secretary Scott Bessent has called for a 50bps cut. Meanwhile, Trump’s appointee Stephen Miran, still awaiting confirmation, could push for even more.

The drama raises questions: Will the Fed board fracture under political pressure? Will Powell assert independence, or will this be his final Jackson Hole?

Beyond September, the path is murky. The market is split on whether we’ll see one, two, or even three more cuts in 2025. Powell might hint at gradual normalisation, especially if he sees inflation as manageable and labour cooling.

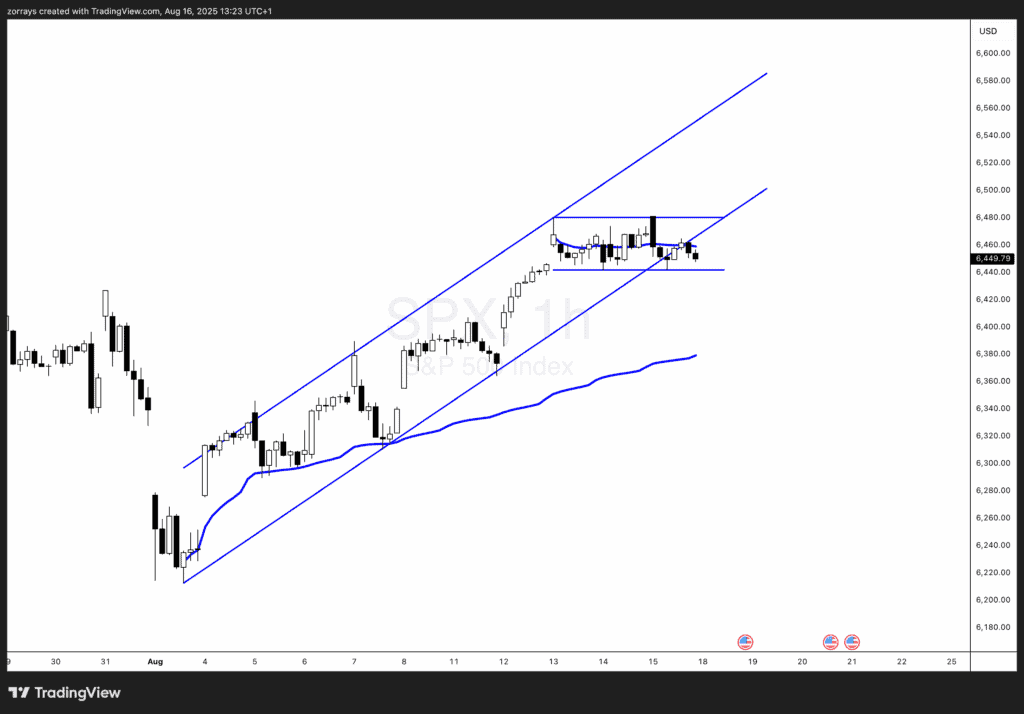

The SPX is currently trading within a well-defined ascending channel, respecting both upper and lower bounds since early August. Price recently consolidated into a parallel channel at the upper end—often a bullish flag continuation pattern.

As long as SPX remains inside this ascending channel, the outlook is mildly bullish. The pullback toward the lower parallel is viewed as healthy consolidation, not breakdown.

Momentum appears to be building for another push higher, especially if Powell delivers a market-friendly tone at Jackson Hole. However, a clean break below the lower blue horizontal support would invalidate this view and shift sentiment near-term.

The ECB and BOE are also near inflection points. A dovish Powell may give them cover to pause. BOJ, meanwhile, remains firmly dovish, offering a contrast that could weaken the yen further.

Political heat, dovish market expectations, and rising internal voices are testing the Fed’s ability to appear neutral and data-driven. Powell’s speech must reassert credibility without spooking markets.

CME FedWatch shows 80% odds of a September cut. Yet real economic indicators suggest caution. Powell could take the opportunity to level-set expectations—especially if the Fed wants to avoid pre-committing.

Watch for:

Institutions appear net long tech and cyclicals, suggesting optimism. But options flows show significant hedging. Expect volatility spikes around the speech window.

It’s an annual economic conference hosted by the Kansas City Fed, bringing together global central bankers, economists, and policymakers.

Markets closely watch Powell’s tone and forward guidance, which often sets the stage for near-term policy moves.

Yes, markets currently price in a high likelihood of a 25bps cut.

Tariffs can raise prices, impacting inflation—a key input into Fed policy. But their long-term effect depends on corporate pricing power and supply chains.

SPX is likely to break higher, especially if it stays in the current ascending channel.

Yes, especially for the ECB and BOE, which often move in sync with the Fed.

With markets pricing in cuts, inflation showing mixed signals, and labor markets wobbling, Jackson Hole 2025 may turn out to be a defining moment for U.S. monetary policy.

For now, the SPX remains in a bullish channel, suggesting optimism prevails—but all eyes are on Powell to either validate or reset expectations.

Alchemy Markets is a multi-asset brokerage providing retail traders with the same elite trading conditions, tools, and transparency typically reserved for institutions.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.