just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

The Federal Open Market Committee (FOMC) meetings are closely watched events, providing critical insights into the Federal Reserve’s views on the economy and their future policy directions. The minutes from these meetings offer a deeper dive into the discussions and considerations that shape monetary policy. The latest FOMC minutes revealed several important developments across financial markets, economic forecasts, and inflation expectations. Let's break down the key points.

For the full report you can visit this link; FOMC Minutes

Developments in Financial Markets and Open Market Operations

The minutes began with a comprehensive review of the recent developments in financial markets. Over the intermeeting period, financial conditions eased slightly, a shift driven by lower long-term interest rates and rising equity prices. It was noted that "current financial conditions appeared to be providing neither a headwind nor tailwind to growth." This neutral stance suggests that while markets are stable, they aren't contributing significantly to economic acceleration or deceleration.

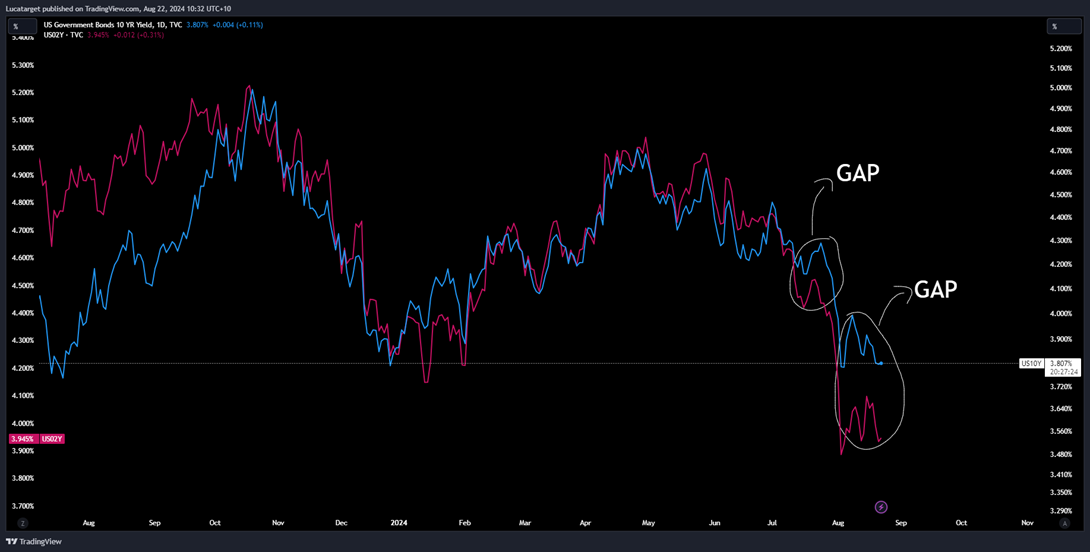

One of the notable shifts was in Treasury yields, where shorter-term yields like the US02Y declined more than their longer-term counterparts like US10Y, leading to a steepening of the yield curve. This change in the yield curve often signals investor expectations of future economic conditions, with sensitivity to economic data such as the Consumer Price Index (CPI) and employment reports remaining high.

US10Y On Blue & US02Y On Pink

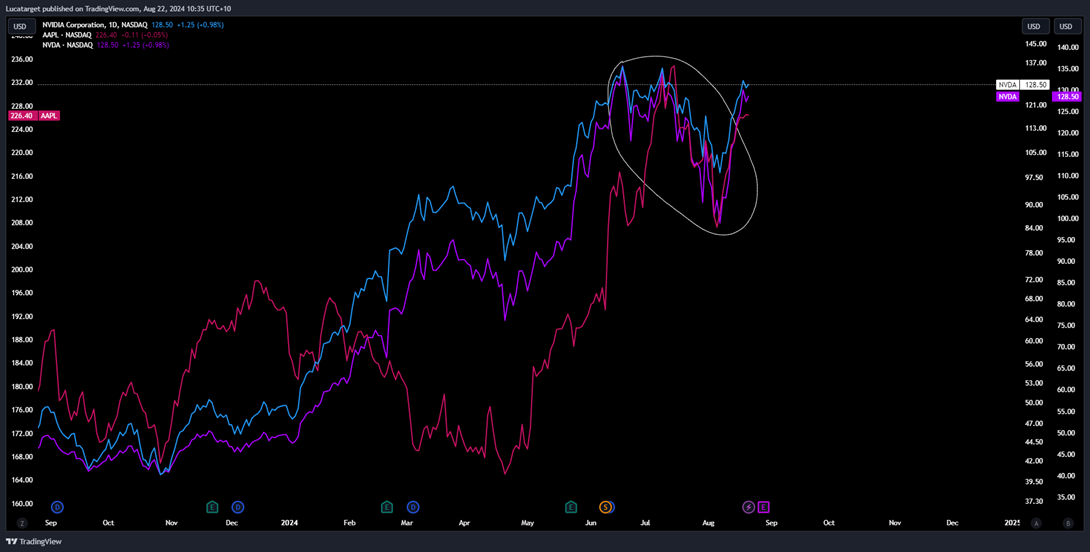

In the equity markets, the anticipation of a September rate cut had a pronounced effect. Stocks of smaller firms, which are more sensitive to interest rates, saw notable gains, while larger companies, particularly in the technology sector, underperformed as we can see with NVIDIA & Microsoft or even Apple. This divergence highlights the varied impact of monetary policy expectations across different market segments.

Apple (Pink), NVIDIA (Blue) & Microsoft (Purple)

On the international front, policy rate expectations in most advanced foreign economies (AFEs) declined, with most central banks expected to ease further. However, the Bank of Japan remained an outlier, with market participants still anticipating a potential tightening of policy.

Money markets also saw minor shifts, with the effective federal funds rate remaining stable, but rates on repurchase agreements (repo) edging higher due to increased demand for financing Treasury securities. The minutes also highlighted the staff's ongoing monitoring of money market developments, with particular attention to the Secured Overnight Financing Rate (SOFR).

Staff Economic Outlook

The economic forecast presented by the staff at the July meeting reflected a somewhat more cautious outlook compared to previous projections. Growth expectations for the second half of 2024 were revised down, largely due to weaker-than-expected labour market indicators. This adjustment narrowed the output gap at the start of 2025, though it remains unclosed.

Over the longer term, through 2025 and 2026, real GDP growth is expected to align more closely with potential, leading to a relatively stable output gap. The unemployment rate is anticipated to rise slightly over the remainder of 2024 and remain steady in the following years.

Inflation expectations were also revised lower, driven by a combination of incoming data and the projected lower level of resource utilization. The staff expects both total and core Personal Consumption Expenditures (PCE) price inflation to decline further, with inflation reaching around 2% by 2026. Despite this more optimistic inflation outlook, the risks are not entirely one-sided. The uncertainty surrounding these projections is considered close to the average of the past 20 years, with risks to inflation still slightly tilted to the upside.

Participants' Views on Current Conditions and the Economic Outlook

The participants in the meeting noted that while inflation has eased over the past year, it remains elevated. They observed that recent disinflation was broad-based across core inflation components, with slowdowns in core goods and housing services. Notably, "participants noted that the recent progress on disinflation was broad based," indicating a more widespread reduction in inflationary pressures.

The discussion also highlighted that firms’ pricing power appears to be waning, with businesses more sensitive to consumer resistance to price increases. This shift is seen as a positive sign that inflation might continue to decline, supported by factors such as moderating economic growth and the reduction of excess household savings accumulated during the pandemic.

Despite these positive trends, some participants expressed caution, noting that inflation pressures could persist due to the economy’s considerable momentum and the still-strong labour market. This divergence of views underscores the complexities involved in predicting the trajectory of inflation and the economy.

The latest FOMC minutes offer a nuanced view of the current economic landscape. While there is optimism around the ongoing disinflation and a stabilizing economic outlook, uncertainties remain, particularly regarding inflation pressures and labour market dynamics. As the Fed continues to navigate these challenges, the insights from these minutes will be crucial in shaping market expectations and guiding future policy decisions.

These developments suggest a cautious yet hopeful path forward, with the Fed keeping a close eye on economic indicators to inform its next moves. As always, the interplay between data and policy will be key in determining the direction of the U.S. economy in the months ahead.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

Why Is Forex Trading So Difficult?![]()

How To Master MT4 & MT5 - Tips And Tricks For Traders![]()

The Importance Of Fundamental Analysis In Forex Trading![]()

Forex Leverage Explained: Mastering Forex Leverage In Trading & Controlling Margin![]()

The Importance Of Liquidity In Forex: A Beginner's Guide![]()

Close All Metatrader Script: Maximise Your Trading Efficiency And Reduce Stress![]()

Best Currency Pairs To Trade In 2024![]()

Forex Trading Hours: Finding The Best Times To Trade FX![]()

MetaTrader Expert Advisor - The Benefits Of Algorithmic Trading And Forex EAs![]()

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.