Search Companies, News, Members & more

Terms of ServicePrivacy PolicySecurity PolicyLegal InformationCommunity GuidelinesSitemapsCookie Settings

2026 Copyright © Liquidity Finder Ltd. All rights reserved.

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Tokenised Money Market Funds

Published on Nov 23, 2025

Updated on Mar 7, 2026

Insight · Tokenised Markets & Collateral

Published: november 23, 2025

Why Buy-Side and Sell-Side Firms Should Care About Tokenised Money Market Funds

Tokenised money market funds (tMMFs) are turning familiar MMF holdings into fast, flexible, yield-bearing collateral – cutting cash drag and laying the groundwork for programmable, automated margin management.

Heineken used to say it “refreshes the parts other beers cannot reach”. In a very similar way, tokenised money market funds (tMMFs) refresh the parts that traditional collateral and legacy payment rails cannot reach.

Tokenisation done right is not a buzzword exercise. It is about enabling things you simply cannot do today, or doing them in a way that is better, faster and cheaper. With tMMFs, buy-side firms can hold yield-bearing assets and still meet collateral requirements on time, while sell-side firms can support clients’ digital asset needs and build new, stickier relationships.

In this article, we look at a live, in-production use case of tMMFs and explain what is in it for you – whether you are on the buy-side or the sell-side.

Key Takeaways

- Same-day title transfer: tMMFs enable same-day movement of high-quality collateral that is often not possible with traditional fund units.

- Minimal documentation changes: in the live use case, a short addendum to an existing ISDA was sufficient.

- Reduced cash drag: buy-side firms can keep capital in yield-bearing MMFs instead of idle cash for margin.

- Path to automation: tokenised collateral creates the foundation for programmable, end-to-end margin and collateral management.

What Are Tokenised Money Market Funds (tMMFs)?

A tokenised money market fund is a conventional MMF whose units are represented as tokens on a distributed ledger. Economically, it is the same conservative, short-duration fund you already know. Operationally, the tokenised version can be transferred, pledged and settled far more quickly and efficiently than its traditional equivalent.

This is where the value lies: tokenisation turns a familiar instrument into high-quality, yield-bearing collateral that moves at the speed of digital assets. Instead of leaving cash idle to cover margin calls, buy-side firms can keep capital working in MMFs while still delivering collateral on time.

The Aberdeen, Lloyds and Archax Live Use Case

A recent live deployment brings the concept into sharp focus. Three firms have combined their roles:

- abrdn (formerly Aberdeen Asset Management), as the asset manager.

- Lloyds Bank, as the major sell-side counterparty.

- Archax, as the regulated digital asset infrastructure provider.

In this set-up, Archax has enabled money market funds managed by abrdn to be tokenised and then used as collateral for FX trades with Lloyds Bank. The underlying fund strategy remains unchanged – what changes is the form factor and mobility of the holdings.

The legacy problem: cash drag and settlement frictions

Any buy-side fund manager with assets in a currency other than the fund’s base currency must manage FX hedging and FX risk. Those hedging trades, typically in the form of forwards, are classed as derivatives and are therefore subject to margining.

In many cases, cash is used to meet variation and initial margin calls because same-day securities transfer is not always possible. That creates “cash drag” – a performance hit from holding non-yielding cash instead of a yield-bearing instrument purely for operational reasons.

The solution: tokenised MMF holdings as collateral

Once the existing MMF holdings were tokenised, abrdn were able to use those tMMFs as a cash substitute for collateral in their existing FX relationship with Lloyds. Critically, this did not require a wholesale legal overhaul:

- A short addendum to the existing ISDA agreement was sufficient to recognise the tokenised MMF units as eligible collateral.

- Operational processes were adapted to recognise same-day title transfer of the tokenised holdings.

The result: abrdn can remain invested in a yield-bearing MMF while still meeting collateral requirements on time, reducing cash drag and improving liquidity management.

Are Tokenised Assets Really Better in This Context?

For this specific use case – collateral for FX hedging – the answer is a clear yes. Tokenising MMF holdings brings several tangible benefits to the buy-side:

- Optionality on investment: stay invested in a yield-bearing asset rather than switching into non-yielding cash purely for margin purposes.

- Reduced cash drag: a smaller cash buffer is needed to service margin calls, freeing more capital to earn a return.

- Same-day title transfer: tokenised MMF units can be moved as collateral on a same-day basis, something not always achievable with traditional fund units.

In other words, tMMFs “refresh the parts” traditional collateral cannot reach – not by changing risk profiles, but by removing operational and settlement frictions that have historically forced firms into holding excess cash.

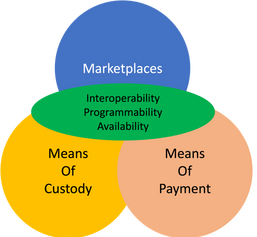

Step One: Interoperability and New Marketplaces

Once an asset is tokenised, interoperability becomes the real enabler. A portfolio manager can:

- Submit buy and sell orders in tokenised MMFs on new marketplaces or venues.

- Immediately use those tokenised holdings as collateral across multiple bilateral and cleared relationships.

These new interactions can be more effective and efficient than today’s siloed processes. Instead of collateral sitting in separate, slow-moving pools, a single, tokenised pool of collateral can be deployed where it is needed, with minimal operational overhead.

Step Two: Programmability and Automated Collateral Management

The next step, already visible but not yet fully mainstream, is programmability. Programmable, tokenised assets make it possible to automate the end-to-end collateral management process.

The calculation engines and risk models we use today can remain broadly the same. What changes is what happens afterwards: the resulting collateral calls and the movement of the collateral itself can be fully automated over “always-on” token rails.

Supporting frequent, intra-day or same-day margin calls becomes straightforward, improving risk management without adding operational headcount. Once again, tMMFs can play the role of yield-bearing, programmable collateral that refreshes parts of the process current infrastructure cannot reach.

What’s In It For Me?

For the Buy-Side

Figure 1: The Holy Trinity v2.0

Figure 1: The Holy Trinity v2.0

If you are on the buy-side and you want more optionality in how you manage collateral, this type of set-up is directly relevant. Key advantages include:

- More flexible collateral: use tokenised MMFs instead of cash to meet margin calls.

- Lower exposure to idle cash: holding a fund or security – whether tokenised or not – is often less risky than holding large, non-yielding cash balances.

- Reduced cash drag: more of your capital remains invested, contributing to performance rather than sitting idle.

For the Sell-Side

If you are on the sell-side, the key question is simple: do we want to support our clients’ digital asset and tokenised collateral needs?

Supporting tokenised money market funds and similar instruments offers:

- First-mover advantage: position your firm ahead of peers who are still thinking purely in terms of legacy collateral processes.

- Deeper client relationships: help clients solve real liquidity and collateral challenges with modern infrastructure.

- New product and revenue lines: from digital custody through to tokenised collateral optimisation and “always-on” margin support.

Think of it like EV charging ten years ago: firms that committed early built brand, loyalty and volume before the rest of the market caught up. The same pattern is now emerging around tokenised assets and tMMFs.

Next Steps

If you are exploring how tokenised collateral and tokenised money market funds could fit into your liquidity and collateral strategy, I would be happy to discuss. Please feel free to get in contact via LiquidityFinder.

Share this article

Comments

Most Recent

Find The Right Partners for

Your Trading Business

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Dark pool trading was once the preserve of institutional desks, but a new wave of AI tools is promising self-directed investors a look into non-displayed liquidity and where the big money sits. This article explains what dark pools actually are, why retail traders face an even bigger information gap in FX than in equities, and what AI-driven intelligence platforms like IUX24 can and cannot reveal about institutional positioning.

SoFi's SoFiUSD is the first stablecoin issued by a US national bank. But do holders actually have the protection they think?

As tokenisation and digital assets move from niche curiosity to mainstream expectation, banks and financial institutions face an uncomfortable truth: their legacy core banking systems were never built for this. From order execution and pre-funding to custody, portfolio management and gas fees, Olaf Ransome explores the key infrastructure challenges FIs must navigate and asks whether to re-use, buy or build their way to a solution that actually scales.

LSEG's DiSH promises atomic settlement and 24/7 PvP and DvP capability using tokenised commercial bank deposits. But when the balances move and the banks don't, who actually owns what? Olaf Ransome examines the mechanics - and the risks.

LiquidityFinder's Sam Low sits down with Nathan Sage, founder and CEO of Sage Capital Management, to trace his journey from FX fund manager to running a Bitcoin fund doing $1BN a day in 2016 — and how that experience of pain built one of the most connected prime brokerages in the digital assets market today.

Klarna is partnering with Coinbase, raising stablecoin-denominated funding and launching KlarnaUSD. We break down the treasury logic, merchant incentives and agentic AI payments angle — and what other CFOs should take from it.

Olaf Ransome’s latest article on liquidity management explores PORTS (Perpetual Overnight Rate Treasury Securities) and how they could expand the supply of on-chain high-quality liquid assets (HQLA) for treasury and cash management. He explains why long cash balances create risk, how stablecoins and tokenised money market funds need safe short-duration assets, and what PORTS could mean for reverse repo, liquidity management and wholesale banking.

African FX liquidity is shaped by hard-currency scarcity and capital controls. Roland Schilling, COO at Sika Financial, explains how interbank reference rates differ from parallel markets, and how Sika settles via CCP/PvP.

Create Your FREE Account

Get access to latest news, updates, real-time data, brokerage and trading firm insights and customized information feeds.

cBridge, by Spotware, has launched Markout Report, a risk intelligence module that lets brokers detect toxic flow, rank accounts by financial impact and act before losses accumulate, all within the bridge.

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

Feed