Search Companies, News, Members & more

Terms of ServicePrivacy PolicySecurity PolicyLegal InformationCommunity GuidelinesSitemapsCookie Settings

2026 Copyright © Liquidity Finder Ltd. All rights reserved.

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

How Tier 1 Providers Shape Institutional Forex Liquidity

Published on Jan 3, 2026

Updated on Jun 22, 2026

Insight

How Tier-1 Providers Shape Forex Institutional Liquidity

Authors: Navneet Giri and Sam Low

Executive SummaryInstitutional FX liquidity is not a single shared pool. A relatively small set of Tier-1 banks and non-bank liquidity providers set prices, manage depth, and control how risk is warehoused. When conditions change at the top of the stack, spreads and execution quality downstream change fast.

On this page

- 1. The Reality of Liquidity

- 2. Who Are the Tier-1 Players?

- 3. The Mechanics: How Tier-1s Shape the Market

- 4. Key Entities and Their Roles

- 5. Trade Lifecycle

- 6. The Data: Why Size Matters

- 7. Technology: The Backbone of Speed

- 8. What This Means for You

- Conclusion

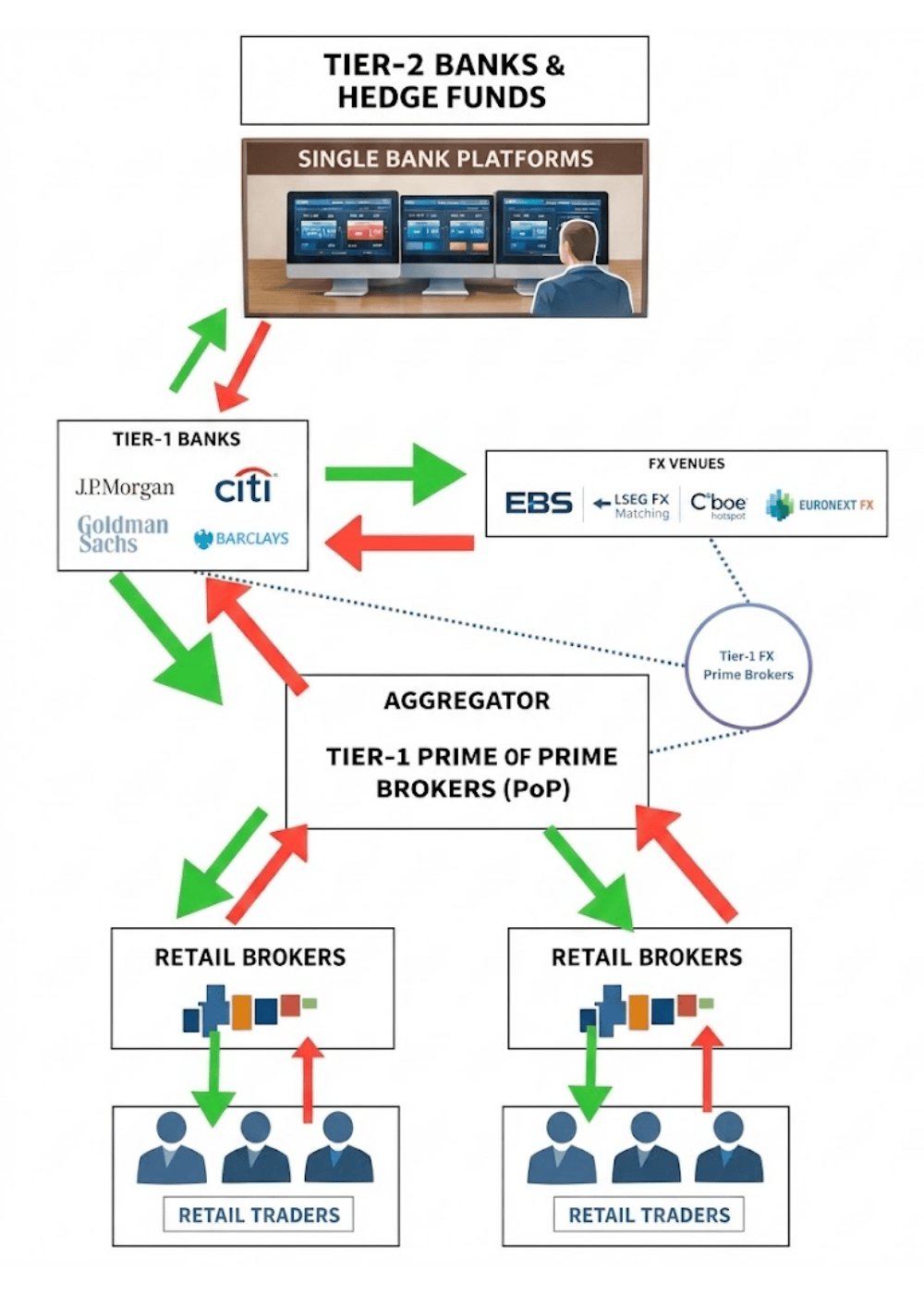

There is a large institutional machine behind every click on a trading terminal. Many participants think of FX as one giant “ocean” of liquidity. In practice, it behaves more like a waterfall: a small group at the top sets the conditions, and everyone downstream consumes that liquidity with incremental mark-ups and constraints.

If you want to understand why spreads widen during news or why a trade slips by a couple of pips, you need to understand what Tier-1 providers are doing at the source.

Image: Overall general structure of the FX market, source: www.liquidityfinder.com

1. The Reality of “Liquidity”

In FX, liquidity is the ability to buy or sell meaningful size immediately without moving the market too far. It is not simply “money in the bank”. It is about executable depth at tight prices.

What liquidity looks like in practice

If you need to sell a large EUR amount, a deep Tier-1 stream may absorb it with limited impact. In thin conditions (for example, late Friday ahead of a holiday), the same order can move price significantly because depth is lower.

Why Tier-1 matters

Tier-1 providers are often the market’s source of truth. Their pricing engines reflect inventory, volatility, and risk appetite. When Tier-1 spreads widen or bids are pulled, the rest of the market tends to react quickly.

Key pointTier-1 institutions do not only “reflect” the market; they help form it by quoting risk, warehousing inventory, and dynamically adjusting spreads and depth based on conditions.

2. Who Are the Tier-1 Players?

“Tier-1” historically referred to major banks. Today it includes a mix of global banks and specialised non-bank liquidity providers (NBLPs) that compete on speed and systematic pricing.

The Global Banks balance sheet + credit

Large banks use their balance sheets to warehouse risk, provide credit, and intermediate client flow at scale.

- Examples: J.P. Morgan, Deutsche Bank, UBS, Citi.

Non-Bank Liquidity Providers (NBLPs) speed + algorithms

NBLPs are typically technology-driven market makers focused on ultra-low latency, systematic models, and scalable electronic pricing.

- Examples: XTX Markets, Citadel Securities, Jump Trading.

FX Market Makers Market Share (illustrative)

| Rank Institution Est. market share (Spot FX) Primary strength | |||

| 1 | XTX Markets | ~10–12% | Algorithmic pricing, reliability |

| 2 | Deutsche Bank | ~9–10% | Deep relationships, balance sheet |

| 3 | J.P. Morgan | ~9–10% | Global reach, credit access |

| 4 | UBS | ~8–9% | Strong eFX stack, consistency |

| 5 | Citadel Securities | ~6–7% | HFT execution, tight majors |

| 6 | Jump Trading | ~5–6% | Ultra-low latency, efficiency |

| 7 | State Street | ~4–5% | Custody flows, real-money volume |

| 8 | Citi | ~4–5% | Corporate hedging, e-platform |

| 9 | Goldman Sachs | ~3–4% | Hedge fund flow, platform depth |

| 10 | Barclays | ~2–3% | Institutional franchise, platform |

Note: Market share can shift over time; the key point is concentration at the top of electronic spot FX.

3. The Mechanics: How Tier-1s Shape the Market

Tier-1 providers actively influence price and depth through a set of well-understood market-making mechanisms.

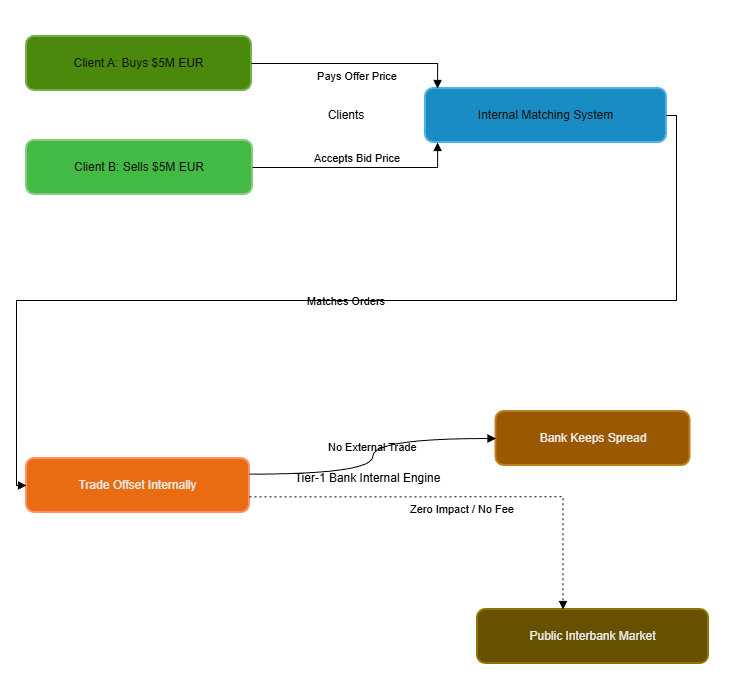

Mechanism A: Aggregation and internalisation

Tier-1 banks receive flow from many counterparties. Rather than hedging every ticket externally, they can internalise matching client orders (buy vs sell) and manage net risk more efficiently. They don't immediately run to the public market to hedge every single one. That would be expensive. Instead they internalise.

If Client A wants to buy $5 million and Client B wants to sell $5 million, the bank just matches them internally. The trade never hits the open market. This allows the bank to collect the spread from both sides without paying any external fees.

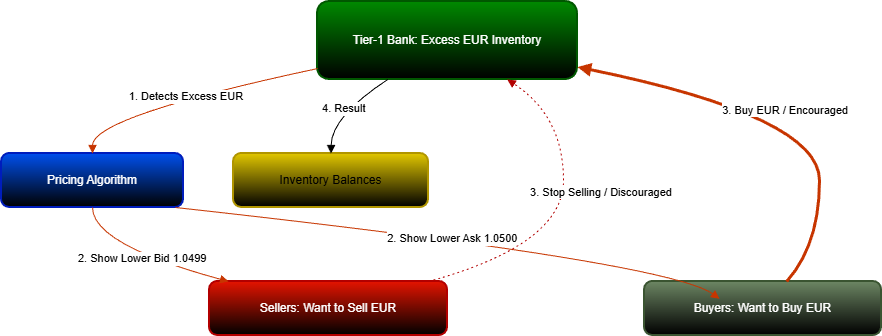

Mechanism B: Price skew (inventory management)

If a bank is long too much of a currency, it may adjust its bid/ask slightly to discourage additional sells and attract buyers, helping rebalance inventory (e.g., they bought too many Euros from clients); they will "skew" their price.

- Normal: 1.0500 (Bid) / 1.0501 (Ask)

- Skewed: 1.0499 (Bid) / 1.0500 (Ask)

By lowering their price slightly, they discourage people from selling to them and encourage people to buy from them. This balances their books. This constant micro-adjustment is what causes the price ticks you see on your chart.

Image: Skewing the price mechanism, source: www.liquidityfinder.com

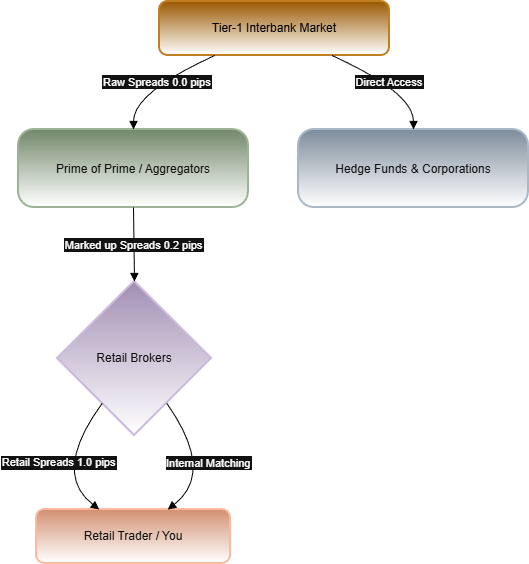

Mechanism C: Recycled Liquidity Down The Chain

Liquidity flows downhill. A Tier-1 bank sells to a "Prime of Prime" (PoP) broker. That PoP broker sells to a Retail Broker. That Retail Broker sells to retail traders.

At each layer, pricing can widen as intermediaries add mark-ups, technology constraints, or risk buffers.

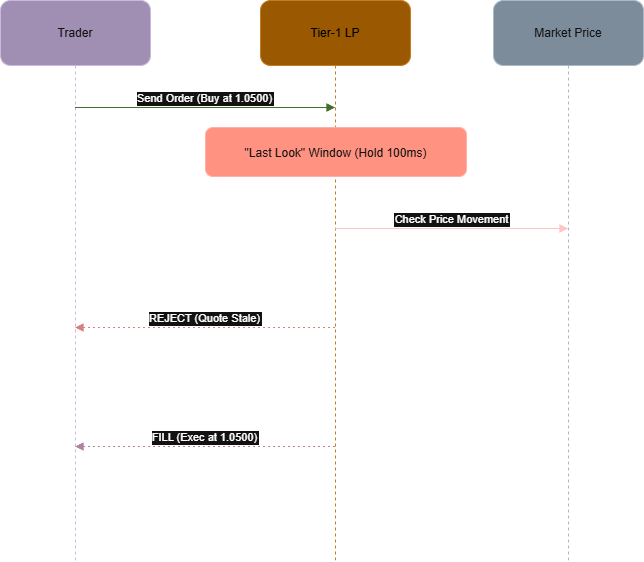

Mechanism D: Last look (controversial)

This is perhaps the most controversial tool in institutional FX. When you send an order to a Tier-1 provider, they often don't fill it instantly. They hold it for a tiny window (usually 5-100 milliseconds) called the "look" window, to decide whether to accept or reject an order. In fast markets, last look can contribute to rejects and slippage.

How it works: If the market moves against the bank during those milliseconds, they reject your trade (claiming the price is "stale"). If the market moves in their favor, or stays flat, they fill it.

・Why they do it: It protects the bank from "latency arbitrage" (traders with faster connections trying to pick off 'stale' prices). Some trading styles (very fast, news-driven, latency arbitrage) tend to trade only when the price is favourable to them and unfavourable to the dealer. Last look reduces that risk. Also, banks often need to offset trades in the market when their risk-book determines this is required (ie they cannot offset the trade internally). Last look gives a tiny window to confirm they can manage the risk at the quoted level.

・Impact on you: This is the primary cause of order rejections and slippage during volatile news events.

Why it’s controversial: it can feel like an unfair “option” for the bank if it’s used to reject trades that would have been profitable for the client

Mechanism E: Ladder (Tiered) Pricing

Liquidity isn't a flat wall; it's a staircase. The price you see on your screen (Top of Book) is usually only valid for a specific volume, anywhere between $100,000 - $1 million. Larger orders can “sweep” multiple depth levels, resulting in a VWAP (Volume Weighted Average Price) that is usually worse than the best displayed price. Remember that prices widen the further down the book you go - this is due to the increased risk for the market-maker for larger sizes.

How it works: If you try to trade $50 million, you "sweep the book." You buy the first $1M at 1.0500, the next $5M at 1.0501, and the final chunk at 1.0503.

Result: Your final execution price is a Volume Weighted Average Price (VWAP), which is always slightly worse than the best price shown. Tier-1 LPs manage these "ladders" dynamically based on volatility.

Image: Ladder (Tiered) pricing mechanism. Source: www.liquidityfinder.com

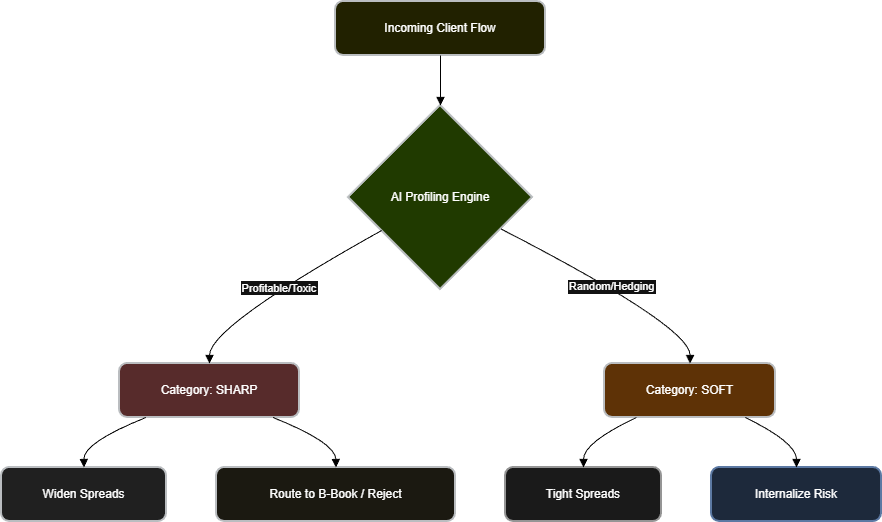

Mechanism F: Client Profiling (Flow Tagging)

Tier-1 providers use sophisticated AI to profile who is on the other side of the trade. They tag client flow into categories, typically "Sharp" (informed/toxic) or "Soft" (uninformed/benign).

'Sharp Flow': Traders who consistently profit or trade milliseconds before a price move. LPs will widen spreads for these clients or route them to a "strictly risk-managed" stream to avoid losses.

'Soft Flow': Corporate hedgers or typical retail flow that is random and less risky. LPs will compete aggressively to get this business, offering tighter spreads because they can easily internalize it for profit.

Image: Client Profiling mechanism, source: www.liquidityfinder.com

How Banks Trade With Each Other

Banks do not just solely rely on thier own customers to understand what the 'market price' is of currencies at any one time. They look for price discovery from the broader market, and there are a few key FX platforms that provide this role.

The major platforms in the interbank market (which are interestingly now owned by the largest global exchange groups) are:

360T (previously independent, now owned by Deutsche Bourse)

Cboe FX (Hotspot) (previously independent, now owned by the Cboe)

CME EBS (previously independent, owned by iCAP, now owned by the CME)

Euronext FX (Fastmatch) (previously independent, now owned by Euronext)

LSEG FX (previously known as Reuters Matching, and was independent until London Stock Exchange Group acquired Thomson Reuters)

These platforms allow banks and non-bank Market Makers to trade with each other anonymously (name given up post-trade) and apply additional liquidity to the market. LiquidityFinder tracks the Average Daily Volumes of these venues on a monthly basis here. These ADV figures act as a proxy for overall FX market activity on a month-by-month basis.

4. Key Entities and Their Roles

This section profiles the giants you need to know. These are the engines powering the industry.

Tier-1 Heavyweights

1. J.P. Morgan

- Role: The world's largest bank by many metrics, JPM is a fortress of liquidity. They provide credit lines that allow other institutions to trade.

- Official URL: jpmorgan.com

- Pros: unmatched stability; huge balance sheet means they rarely "turn off" during crises.

- Cons: difficult to access directly unless you have $50M+ in capital; can be slower to adopt new tech than NBLPs.

2. XTX Markets (Non-Bank Market Maker)

- Role: A quantitative trading firm that has disrupted the banks. They use code, not humans, to make markets. They are often the #1 liquidity provider globally for Spot FX.

- Official URL: xtxmarkets.com

- Pros: incredibly tight spreads; consistent pricing even during volatility; no human bias.

- Cons: they are purely electronic—you can't call a broker there to "work an order" for you.

3. Deutsche Bank (Autobahn)

- Role: Historically the king of FX. Their electronic platform, "Autobahn," set the standard for institutional trading.

- Official URL: cib.db.com

- Pros: deep liquidity in complex pairs (not just majors); massive research and data capabilities.

- Cons: has lost some market share to NBLPs in recent years; legacy technology hurdles.

4. UBS

- Role: A Swiss giant that has been a dominant force in FX for decades. Their "Neo" platform is a staple on institutional desks.

- Official URL: ubs.com/global/en/investment-bank

- Pros: Extremely reliable technology; dominant liquidity in Swiss Franc (CHF) pairs; strong prime brokerage services.

- Cons: Can be very conservative with credit lines; rigorous onboarding process.

There are just some of the top names commonly accepted as the top market makers in FX by volume. To see the 'league tables' of FX banks by volume, usually the industry refers to Euromoney who follow this closely, although a paid subscription is usually required to see their research.

FX Prime Brokerage

Prime of Prime (PoP) FX providers sit between Tier-1 liquidity and the wider market by using prime brokerage (PB) relationships to “rent” balance sheet and credit. In practice, a PoP establishes a PB line with a Tier-1 bank and then uses that prime relationship to face multiple Tier-1 liquidity streams (and venues) on institutional terms. The PoP then repackages this access for downstream brokers, funds, and professional traders by combining credit intermediation + aggregation + connectivity: they consolidate pricing from several Tier-1 banks/NBLPs into a single feed, apply pre-trade risk controls, and offer clients executable streams without each client needing to clear the Tier-1 bank’s credit and onboarding hurdles individually.

The reason this model exists is the collateral and credit intensity of prime brokerage. A Tier-1 bank prime broker (including banks such as NatWest or Standard Chartered) will typically require a material, ongoing collateral commitment under robust legal documentation (prime brokerage agreement + margin terms), with eligible collateral often limited to cash and high-quality liquid collateral. The exact requirement varies by counterparty strength, regulatory status, expected volumes, and flow characteristics, but for many market participants the “real” hurdle is that meaningful PB limits tend to be supported by large, continuously available balances. These are usually high seven-figure to eight-figure USD.

This makes direct Tier-1 access uneconomic or unattainable for many firms, which is why PoPs—who can post and manage that collateral centrally—become the practical route into Tier-1 pricing for the second tier. The names we most often hear at LiquidityFinder being used by Prime of Primes for FX Prime Brokerage are NatWest Markets (who seem to have one of the lowest barriers to entry) and Standard Chartered.

Prime of Prime providers and institutional brokers can intermediate access by aggregating liquidity, credit, and connectivity.

The Bridge Builders (Prime of Prime)

Many participants cannot access Tier-1 venues directly. There is a very-high barrier to entry to obtain the prices from Tier-1 banks directly because it is credit-gated, not just connection-gated.

Direct access typically requires:

(i) counterparty credit approval and ongoing limits,usually in the $10's of millions of dollars in collateral/balance sheet

(ii) extensive KYC/AML, sanctions and governance checks,

(iii) institutional-grade technology and controls, and

(iv) sufficient scale to justify the relationship economics.

For many firms, they have to meet the bank’s combined requirements across risk, compliance, legal documentation and operational readiness.

The way other firms at the second tier access these prices is via a Prime Brokerage relationship. Many institutional Tier-2 'Prime Brokers' more commonly known as 'Prime of Primes' have emerged over the past few years. These firms can leverage their Tier-1 bank Prime Brokerage relationships to gain access to the Interbank Tier-1 FX market and can pass this liquidity downstream to medium/small-sized asset managers, Retail Brokers and professional traders. These PoPs need to aggregate the multiple sources of Bank/Non-Bank liquidity they have access to via FX aggregators such as Integral or FXSpotStream.

GCEX

Role: GCEX is a digital prime brokerage and liquidity/technology provider offering institutional access across FX and multi-asset markets, focused on bridging clients into deeper liquidity relationships and institutional workflows.

Pros: Multi-asset capability alongside FX; institutional “plug-in” style offering that can combine brokerage, liquidity and connectivity. GCEX operates on a pure A-book model, or Agency model, meaning that every trade is passed to its Tier-1 LPs for execution. GCEX does not take on any risk from its clients trading.

Cons: Broader digital-prime scope can be more than FX-only firms need; onboarding and suitability can be stricter than lighter-touch liquidity providers. Relatively limited if looking for broad multi-asset solutions including single-stocks CFDs.

MAS MarketsRole: MAS Markets is an institutional liquidity provider offering FX (and typically broader multi-asset) liquidity and technology solutions designed for brokers and professional clients.

Pros: Institutional positioning with a broker-focused offering; can be a practical route to aggregated liquidity and execution infrastructure without direct Tier-1 onboarding. MAS Markets operates on a pure A-book model, or Agency model, meaning that every trade is passed to its Tier-1 LPs for execution. MAS Markets does not take on any risk from its clients trading.

Cons: Not a Tier-1 balance-sheet bank—pricing/capacity depends on underlying LP mix and your flow profile; minimums and due diligence can exclude smaller firms.

ADMISI eFX (ADM Investor Services International)Role: ADMISI eFX is the electronic FX division of one of the world's oldest and largest commodities houses, providing access to a network of bank and non-bank liquidity across FX (often including deliverable FX and NDFs) and related products such as precious metals. ADMISI eFX is an A-book, agency broker, meaning it dies not take any risk or hold positions from its clients' trades, passing every trade to its tier-1 bank and non-bank liquidity providers.

Pros: Broad liquidity network and product breadth beyond simple spot; institutional brokerage infrastructure and client service model.

Cons: More “brokerage access + network” than a pure low-latency market maker—execution experience can vary by stream, size, and client profile; onboarding follows institutional standards.

ATFX Connect (ATFX ConnectX)Role: ATFX Connect is an institutional liquidity provider (PoP-style) that aggregates liquidity from bank and non-bank sources and distributes streams to brokers and professional counterparties. In September 2025, ATFX launched ATFX ConnectX to provide access to the various Tier-1 interbank venues through a single prime-brokerage credit set-up.

Pros: Single onboarding route to a multi-source pool; flexibility in stream formats (e.g., sweepable vs full-amount) depending on setup. Can provide access to the interbank FX market venues.

Cons: As with all PoPs, outcomes depend heavily on stream selection and routing—firms should diligence last-look policy, reject rates, mark-ups and transparency per feed.

Britannia Global MarketsRole: Britannia Global Markets is a London-based multi-asset brokerage providing institutional FX access (often including deliverable FX and NDFs) alongside broader derivatives and prime-services style connectivity.

Pros: Institutional distribution model with a relationship-led approach; product breadth for clients needing more than spot FX.

Cons: Typically not a “self-serve” liquidity relationship—documentation, onboarding timelines and minimums can be heavier than pure electronic providers.

Equiti CapitalRole: Equiti Capital is a London-based liquidity provider offering tailored FX and CFD liquidity solutions for professional and eligible counterparties, commonly delivered via FIX and broker technology stacks. Equiti Capital use the services of Tier-1 Prime Brokers such as NatWest Markets.

Pros: Broker-friendly integration approach; flexible, bespoke liquidity setup suited to professional flows and brokerage use-cases.

Cons: More broker-liquidity/CFD-oriented than interbank venue access; best fit is usually broker/professional flow rather than direct-style Tier-1 dealing.

StoneX ProRole: StoneX Pro is the institutional FX offering of StoneX, providing FX trading and liquidity solutions spanning spot and typically broader OTC products (e.g., forwards, swaps, NDFs, options), often combining internal market making with bank liquidity. Usually works with commercial type clients than retail brokers.

Pros: Wide product coverage for firms that need more than spot; “one counterparty/one connection” operational simplicity; strong group backing. Utilises Tier-1 Bank LPs.

Cons: Breadth can mean less single-purpose optimisation for ultra-tight spot-only execution; terms and coverage can vary by entity/jurisdiction and client classification.

Sucden Financial

Role: Sucden Financial is a London-based brokerage with deep roots in commodities and futures, providing institutional market access across FX and listed/OTC products with a mix of electronic execution and traditional brokerage support.

Pros: Strong heritage and balance across asset classes, particularly commodities; ability to support more complex or relationship-driven execution alongside electronic pricing.

Cons: More relationship-led and “old school” than pure electronic NBLPs; not positioned as a single-product, ultra-low-latency spot FX market maker.

FXCM Prime

Role: FXCM Prime is an institutional prime-of-prime style liquidity provider offering aggregated multi-asset liquidity and execution services for brokers, funds and professional counterparties, typically delivered via FIX and integrated with common brokerage technology stacks. FXCM Prime can provide sponsored access to the interbank FX venues at a relatively low barrier to entry in terms of collateral.

Pros: Broker-friendly onboarding route to a multi-LP pool; operationally convenient “one connection” model; experience supporting institutional-style execution workflows (pricing, risk controls, reporting). Can provide access to Tier-1 FX venues.

Cons: As with any PoP, realised execution quality depends on the underlying LP mix, routing and your flow profile—firms should diligence mark-ups, last-look/reject behaviour, and stream transparency before scaling.

LMAX Exchange

Role: London-based LMAX Exchange operates an institutional exchange (MTF) for FX, providing a central limit order book.

Pros: High transparency with limit order book visibility; no "last look" execution.

Cons: Market data fees apply; cost structure favors larger volume players. Slippage seems to be something we hear about users experiencing with LMAX.

SwissquoteRole: Swissquote is a Swiss banking group offering deep institutional liquidity and custodial services.

Pros: Tier-1 bank safety and stability; huge balance sheet; regulated in Switzerland (FINMA). Use Tier-1 banks as Prime Brokers.

Cons: Conservative leverage limits; rigorous and slow onboarding process.

26 Degrees Global Markets (formerly Invast Global)Role: 26 Degrees (formally Invast Global) is an APAC-focused prime broker specializing in multi-asset prime services.

Pros: Exceptional liquidity in JPY and Asian pairs; strong support in Sydney time zone. Parent is regulated by the Japanese FSA so is under stringent regulatory control. 26 Degrees utilise Tier-1 Prime Brokers.

Cons: Less focus on US/EU clients compared to global banks.

iSAM Securities (formerly IS Prime)

Role: iSAM Securities (formerly IS Prime) is a quantitative-driven technology and liquidity firm born from a hedge fund (iSAM).

Pros: Superior analytics and technology; built by quants for quants; excellent risk management tools. Utilise Tier-1 banks as Prime Brokerage access to Tier-1 liquidity. Have a broad range of Retail Broker clients.

Cons: Niche focus; strict counterparty requirements.

FinaltoRole: Finalto (formally CFH Markets) is a significant name in the B2B liquidity space for retail brokers and smal/medioum sized asset managers. Also a tech provider offering a one-stop-shop for brokers.

Pros: Huge multi-asset range in addition to FX, including CFDs and equities; integrated tech and liquidity. The majority of their flow hits the 'street' to Tier-1 banks and PBs.

Cons: Finalto's minimum regulatory capital requirements and stringent onboarding may mean some brokers in the lower tier jurisdictions will find it hard to be onboarded here.

CMC Markets Connect

Role: CMC Markets Connect is the institutional arm of the UK-listed retail trading giant, leveraging their proprietary tech for B2B clients.

Pros: Publicly listed (FTSE 250) transparency; deep liquidity in indices and FX. Utilise Tier-1 Prime Brokers and their liquidity is now unique, meaning they appear in some of the majoe Tier-1 venues as an independent 'unique' price, and not 'recycled' interbank liquidity.

Cons: Primarily known as a retail brand; platform is proprietary (not MT4/5 native). It is possible that their servers are not co-located in LD4 but may be in house in the London HQ, although this mayhave changed recently.

Scope Prime

Role: Scope Prime is an institutional liquidity, trading and fintech solutions provider for brokers, hedge funds and professional counterparties, offering multi-asset market access supported by proprietary liquidity aggregation and API-driven execution workflows.

Pros: Strong “one-provider” institutional stack (liquidity + aggregation + platforms/APIs) aimed at brokers and professional flows; broad tradable-asset coverage and an infrastructure-led approach designed for low-latency, electronic execution. Scope Prime can provide clients with access to market-making banks, "facilitated by leading electronic trading platforms EBS Market and Refinitiv Matching."

Cons: More multi-asset/brokerage-and-solutions oriented than a pure interbank spot FX venue—best fit is typically professional/broker flow where operational setup, reporting and controls matter, rather than firms seeking a direct Tier-1 bank-style relationship.

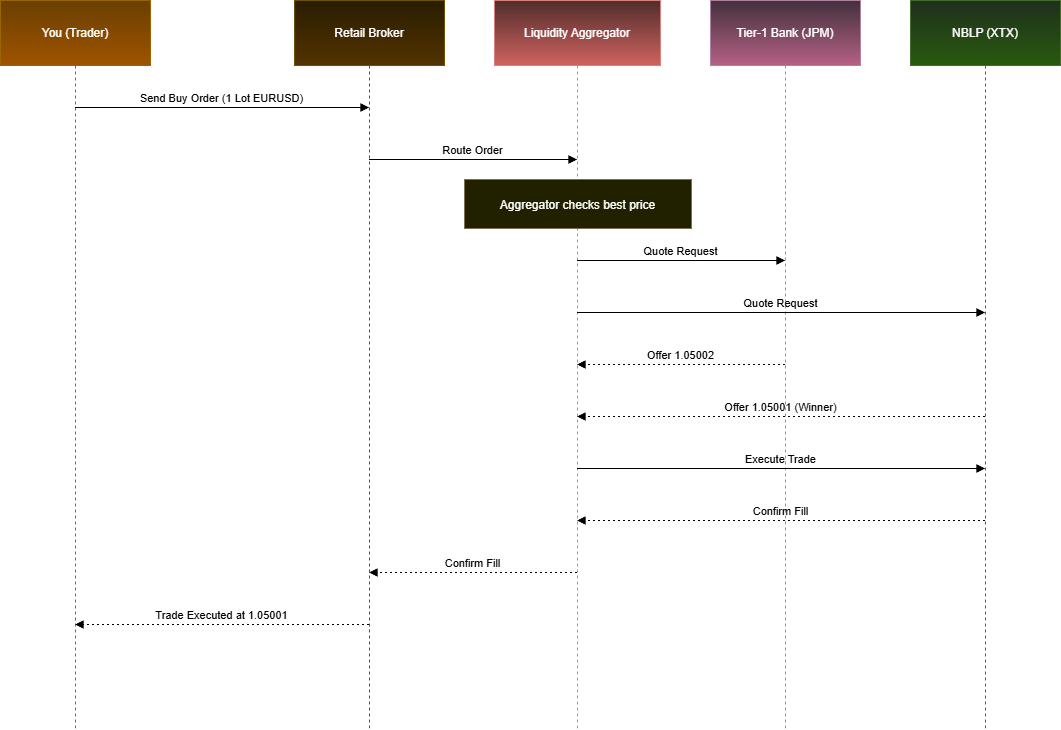

5. Trade Lifecycle

When you click “Buy”, your order routes through technology and counterparties in milliseconds. The route (direct Tier-1 access vs multiple intermediaries) can change spread, rejection rates, and realised fill/execution price.

Image: Visualization of trade lifecycle, source: www.liquidityfinder.com

6. The Data: Why Size Matters

The FX market trades roughly $9.6. trillion per day (BIS 2025 Triennial Survey). Concentration at the top can deliver efficiency, but it can also reduce resilience during stress. Here is the statistic that matters:

The Top 5 Dealers control ~45% of all volume.

Concentration matters: When a small number of dominant providers widen spreads or reduce quoting, downstream liquidity can degrade quickly.

This concentration of power is a double-edged sword.

The Good: It creates massive efficiency. With so much volume going through so few hands, spreads on EUR/USD can be as low as 0.0 pips at the institutional level.

The Bad: It creates "Liquidity Mirages." In 2015, during the Swiss Franc crash, liquidity evaporated because the few major banks providing it all pulled their plugs at the same time. When the top 5 stop quoting, the market stops moving.

Latency Metrics (illustrative)

Average human reaction: ~250ms

Typical retail broker execution: ~100–300ms

Tier-1 execution speed: often < 5ms

If your broker is slow, the price has already changed 50 times before your order even reaches the market. This is why "slippage" happens.

While FIX API (Financial Information exchange) is the industry standard language that allows these banks to "talk" to each other, it is just one layer of the tech stack. The true battle for liquidity happens on multiple fronts.

1. Protocols: FIX vs. Binary (ITCH/OUCH)

・FIX API (The Standard): This is a text-based protocol. It is reliable and flexible, used for most reporting and standard trading. However, because it is text, it takes slightly longer for a computer to "read" (parse) it.

・Binary Protocols (The Speed Demons): High-frequency firms (like XTX or Citadel) often prefer binary protocols like ITCH (for market data) and OUCH (for order entry). These are stripped-down, numeric codes that are much harder for humans to read but incredibly fast for machines to process.

2. Hardware Acceleration (FPGA)

Software is becoming too slow for the top tier.

・What it is: FPGA (Field-Programmable Gate Array) is a special type of microchip.

・How it works: Instead of running trading software on an operating system (like Windows or Linux), the trading logic is "hardwired" directly onto the chip itself.

・Result: This reduces processing time from microseconds (millionths of a second) to nanoseconds (billionths of a second).

3. Smart Order Routers (SOR)

This is the "brain" of the liquidity aggregator.

Function: When you send a large order, the SOR breaks it into tiny pieces. It scans all available venues (Banks, ECNs, Dark Pools) and sends the pieces to different places instantly to get the best overall price without alerting the market.

4. Physical Connectivity (Cross-Connects)

Where does this happen? It happens physically in massive, fortress-like data centers.

・NY4 (New York/Secaucus): The hub for US equities and dollar-based pairs.

・LD4 (London/Slough): The hub for European pairs.

・TY3 (Tokyo): The hub for Asian pairs.

The "Cross-Connect":

Serious traders don't just use the internet. they lease a server rack inside these data centers. They then run a physical yellow fiber-optic cable (a cross-connect) directly from their server to the bank's server in the next cage.

- Why? To eliminate the travel time of light across the city. If the cable is shorter, the data travels faster.

8. What This Means for You

You might be thinking, "I trade $1,000 accounts, why do I care about J.P. Morgan's servers?"

Here is why: Your broker's liquidity source determines your profitability.

1) The "B-Book" Risk: If your broker doesn't have good relationships with Tier-1 providers, they might just "B-Book" you. This means they take the other side of your trade. If you win, they lose. This creates a conflict of interest.

2) News Spikes: During a Non-Farm Payroll (NFP) release, Tier-1 providers widen their spreads to protect themselves. If your broker has poor technology, those spreads widen even more for you, triggering your stop-loss unnecessarily.

3) True ECN vs. Fake ECN: Many brokers claim to be ECN (Electronic Communication Network). A true ECN broker aggregates prices from multiple Tier-1 LPs (like in the diagram above) and gives you the best one. A fake one just simulates this.

Actionable Advice:

Ask your broker who their liquidity providers are. If they can't or won't tell you, that is a red flag. Legitimate brokers are proud to list "Liquidity from Top Tier Banks" on their site.

Conclusion

The forex market isn't a democracy; it's a hierarchy. Tier-1 providers like J.P. Morgan, XTX Markets, and Deutsche Bank sit at the top, creating the river of money that we all fish in. They use immense capital and lightning-fast technology to keep spreads tight and markets moving.

Understanding this structure helps you realize that trading isn't just about reading charts. It's about understanding who is on the other side of the screen. When you see a price on your screen, it's the end result of a high-speed war between algorithms, credit lines, and risk management engines.

Choose a broker that has a direct line to these giants, and you will be trading on a much firmer foundation.

Disclaimer: This article is for informational purposes only and does not constitute investment, legal, tax, or trading advice.

Found this interesting? Become a member of LiquidityFinder and get daily industry news direct to your inbox — join here.

Author

| Navneet Giri - Navneet is a professional quantitative trader with extensive experience in derivatives trading across major global exchanges and financial markets, including cryptocurrencies. | He employs market-making strategies and participates in liquidity enhancement programs to achieve optimal trading results. |

Author

| Sam Low is the Founder of LiquidityFinder. With over 18 years in working with FX trading technology, Sam has deep experience in the FX (forex) trading industry, working with brokers, liquidity providers and end traders themselves. | You can message Sam directly here. |

What does “Tier-1 liquidity” mean in FX? +Tier-1 liquidity refers to pricing and executable depth coming from the very top of the institutional FX stack—typically major global banks and the largest electronic non-bank market makers. These providers form the tightest prices and the most reliable depth in normal conditions, and their risk appetite heavily influences what everyone downstream receives.

Why do spreads widen during major news events? +Spreads widen when volatility spikes because market makers face higher risk of adverse selection (being “picked off” by faster traders) and larger, faster price moves. Tier-1 providers protect themselves by widening spreads, reducing quote size, or pulling quotes temporarily. Downstream providers often widen further because they add mark-ups and risk buffers on top of already-wider Tier-1 prices.

What is “last look” and why is it controversial? +Last look is a brief window (often milliseconds) where a liquidity provider can accept or reject a trade after receiving it, typically to protect against stale pricing and latency arbitrage. It’s controversial because it can feel like an unfair “option” for the dealer if rejects rise in fast markets or if fills consistently disadvantage the client. The right way to judge it is by monitoring reject rates, slippage distribution, and whether execution rules are transparent and consistent.

What’s the difference between Tier-1 banks and non-bank market makers (NBLPs)? +Tier-1 banks bring balance sheet, credit, and prime brokerage capabilities—meaning they can extend credit lines and support large-scale institutional relationships. Non-bank market makers focus on speed, algorithms, and systematic pricing, often competing aggressively in spot FX majors with ultra-tight spreads. Many institutional liquidity pools combine both because they complement each other: banks provide credit and breadth; NBLPs provide highly efficient electronic price-making.

Why can’t most firms access Tier-1 FX pricing directly? +Direct Tier-1 access is credit-gated, not just tech-gated. It usually requires stringent counterparty onboarding (KYC/AML, sanctions, governance), legal documentation, institutional-grade controls, and meaningful scale. Most importantly, it requires sufficient credit support and collateral capacity to justify a direct relationship and trading limits with a top-tier bank.

What is a Prime Broker (PB) in FX, and what do they actually provide? +A prime broker is typically a Tier-1 bank that provides credit intermediation, settlement, and access to institutional FX liquidity under the bank’s umbrella. With PB, the client can trade with multiple liquidity providers while the prime broker sits in the middle for credit and settlement. This structure is widely used in institutional FX because it streamlines access while centralising risk, margining, and operational controls.

What is a Prime of Prime (PoP), and why do brokers use them? +A Prime of Prime sits between Tier-1 prime brokerage and the rest of the market. PoPs use their own prime brokerage relationships to access Tier-1 liquidity, then distribute aggregated pricing to brokers, funds, and professional traders who can’t meet Tier-1 PB requirements. Brokers use PoPs to get “one connection” access to multiple liquidity sources, plus help with credit intermediation, risk controls, and operational support.

What is “ladder” (tiered) pricing and why does size change your fill price? +Top-of-book pricing is usually only valid up to a certain size. Larger orders consume liquidity across multiple price levels (depth), producing a volume-weighted average price (VWAP) that is typically worse than the best displayed quote. Tier-1 providers continuously adjust these depth ladders based on volatility, inventory, and expected market impact—so the bigger you trade, the more you need to think about market impact and routing.

What does “toxic flow” mean, and how does it affect execution? +“Toxic” (or “sharp”) flow is order flow that tends to be informed or latency-advantaged—meaning it arrives just before prices move, causing consistent losses for liquidity providers. Tier-1s and NBLPs profile flow and may respond by widening spreads, reducing size, increasing rejects, or placing clients on stricter streams. If a broker’s client base is heavily skewed toward sharp flow, execution quality can degrade even if the broker has strong liquidity sources.

How can I tell if my broker’s liquidity and execution are institutional-grade? +Ask specific questions: Who are your liquidity providers? Is execution last look or firm? What are typical reject rates during volatility? Do you aggregate multiple LPs or rely on one stream? Can you share execution statistics (slippage distribution, fill ratios, latency)? Strong brokers are usually transparent about their model, can explain routing and controls clearly, and can demonstrate consistent execution quality—especially during fast markets.

Share this article

Comments

Most Recent

Find The Right Partners for

Your Trading Business

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Dark pool trading was once the preserve of institutional desks, but a new wave of AI tools is promising self-directed investors a look into non-displayed liquidity and where the big money sits. This article explains what dark pools actually are, why retail traders face an even bigger information gap in FX than in equities, and what AI-driven intelligence platforms like IUX24 can and cannot reveal about institutional positioning.

Risk and dealing analytics provider BrokerPilot helps multi-asset brokers spot toxic flow before it eats into their P&L. Chief Revenue Officer Sergey Berezhnoy talks to Sam Low about catching toxic patterns across MT4, MT5 and cTrader, why new brokers get targeted from day one, and where AI fits into the dealing room without replacing the human dealer.

LSEG's DiSH promises atomic settlement and 24/7 PvP and DvP capability using tokenised commercial bank deposits. But when the balances move and the banks don't, who actually owns what? Olaf Ransome examines the mechanics - and the risks.

Klarna is partnering with Coinbase, raising stablecoin-denominated funding and launching KlarnaUSD. We break down the treasury logic, merchant incentives and agentic AI payments angle — and what other CFOs should take from it.

Olaf Ransome’s latest article on liquidity management explores PORTS (Perpetual Overnight Rate Treasury Securities) and how they could expand the supply of on-chain high-quality liquid assets (HQLA) for treasury and cash management. He explains why long cash balances create risk, how stablecoins and tokenised money market funds need safe short-duration assets, and what PORTS could mean for reverse repo, liquidity management and wholesale banking.

African FX liquidity is shaped by hard-currency scarcity and capital controls. Roland Schilling, COO at Sika Financial, explains how interbank reference rates differ from parallel markets, and how Sika settles via CCP/PvP.

In Part 3 of his A-Book STP series, Youssef Bouz explains why STP should be viewed as a trading environment—not a feature—exploring execution realism, market behaviour, and why professional and algorithmic traders prefer true STP models for long-term alignment and scalability.

Guest insight from Olaf Ransome on UNITE Global FMI and a “single pool of liquidity” vision to reduce nostro reliance, cut buffers and enable real-time PvP/DvP.

Create Your FREE Account

Get access to latest news, updates, real-time data, brokerage and trading firm insights and customized information feeds.

Spotex has appointed Joe Tuccio, previously Head of Digital Partnerships at Seabury Capital, as Head of Digital Assets. Tuccio brings 20 years of financial markets experience and will lead partnerships with liquidity providers and custodians as Spotex expands its institutional FX venue into digital assets.

RoboForex has integrated its MobileTrader platform into Telegram as a Mini App, giving traders account management, order execution, analytics and copy trading access within the messaging platform, with real-time synchronisation across Telegram, iOS, Android and web versions.

Learn how deliberate practice can improve your trading skills faster than spending more time on the charts. Discover practical tips to build discipline, consistency, and long-term trading success.

XS.com has appointed Anna Pastusenco as Group PSP and Banking Manager, tasking her with leading global payment partnerships across banks, EMIs and PSPs. She joins from IC Markets, bringing experience in payment infrastructure, banking relationships and commercial negotiations to the global broker's expanding payments ecosystem.

Looking at the latest Gold XAU/USD price action? See why a bearish trend continuation point to a massive drop.

Want to learn how to trade ECB events? Discover the top strategies for ECB announcement days, including volatility trading and breakout tactics.

Darwinex has integrated with TradingView, letting traders on the charting platform build a verified, publicly auditable track record from every trade. The move links Darwinex's regulated broker and Darwinex Zero development platform to investor capital allocation, based purely on trading performance.

Pepperstone has appointed Mohammed Almadhoun as Head of Middle East and Osama Hamdan as Head of Sales, strengthening its regional leadership team as the FX and CFD brokerage continues its expansion across the UAE, GCC and wider MENA region following its Dubai office launch.

Payments company Stripe and private equity group Advent International have launched a joint offer to acquire New York-listed payments group PayPal in a deal that would value the business at around $53bn, according to the Financial Times.

ATFX has launched the World Trading Cup, a three-stage trading competition offering up to USD 210,000 in prizes. Pre-registration opens 20 July 2026, with regional qualifiers and finals leading to a global final in December, where 15 traders from five regions will compete for the championship title.

Feed