Search Companies, News, Members & more

Terms of ServicePrivacy PolicySecurity PolicyLegal InformationCommunity GuidelinesSitemapsCookie Settings

2026 Copyright © Liquidity Finder Ltd. All rights reserved.

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

How Sika's New FX Platform Simplifies Emerging Market FX Order Matching

Published on Nov 25, 2025

Updated on Mar 7, 2026

How SIKA’s New FX Platform Simplifies EM FX Order Matching & Settlement

SIKA Financial Group is launching a new FX platform designed to make emerging-market (EM) FX order matching and settlement safer, more efficient, and easier to scale for banks, corporations, brokers, and real-money institutions.

Key Takeaways: EM FX Order Matching, Liquidity & Settlement

▪️ EM currencies typically sit outside CLS and lack PvP (Payment versus Payment), increasing settlement and credit risk for EM FX flows.

▪️ SIKA’s central counterparty (CCP) model enables multilateral netting, pre-funded settlement and same-day recycling of balances back to clients’ local Nostro accounts.

▪️ The platform supports both fiat and digital currencies, including stablecoins, with a roadmap towards true atomic netting and settlement as Web 3.0 rails mature.

The Challenge of EM FX Liquidity & Settlement

Foreign exchange liquidity is a very big business. Settlement of FX currencies is also a big thing, but often far from being an easy thing, particularly in EM currencies. For one thing, EM currencies do not settle in CLS, so there is no PvP (Payment vs. Payment) mechanism. So, at the very least, settling EM trades typically incurs credit and settlement risk, with associated operational pain and delay. As such, when a new platform comes along suggesting it can remove EM FX settlement pain points and reduce associated risks, it is worth giving it some attention.

When a new EM FX platform claims it can reduce settlement pain points and associated risks, it is worth a closer look. Before exploring SIKA’s new model, it helps to recap how non-PvP, non-CLS FX settlement generally works today.

Three Common Non-PvP FX Settlement Models

1) Gross settlement with full settlement risk

Each FX trade settles individually. One party makes a payment without knowing whether the counterparty, often in a different time zone, has made the corresponding payment. Settlement and credit risk are fully borne between the two parties.

2) Bi-lateral netting at currency pair level

Counterparties agree a net amount per currency. This reduces gross settlement flows but there is still residual credit and settlement risk if one side fails.

3) “Safe” settlement via pre-funding

Liquidity providers and major banks, especially in EM currencies, may insist that clients pay first. Only once funds are received and reconciled is the offsetting payment released. This is manual, cumbersome and slow. It is widely used in Africa, where a handful of major South African banks often dominate EM FX settlement because they invest in understanding the underlying credit risks.

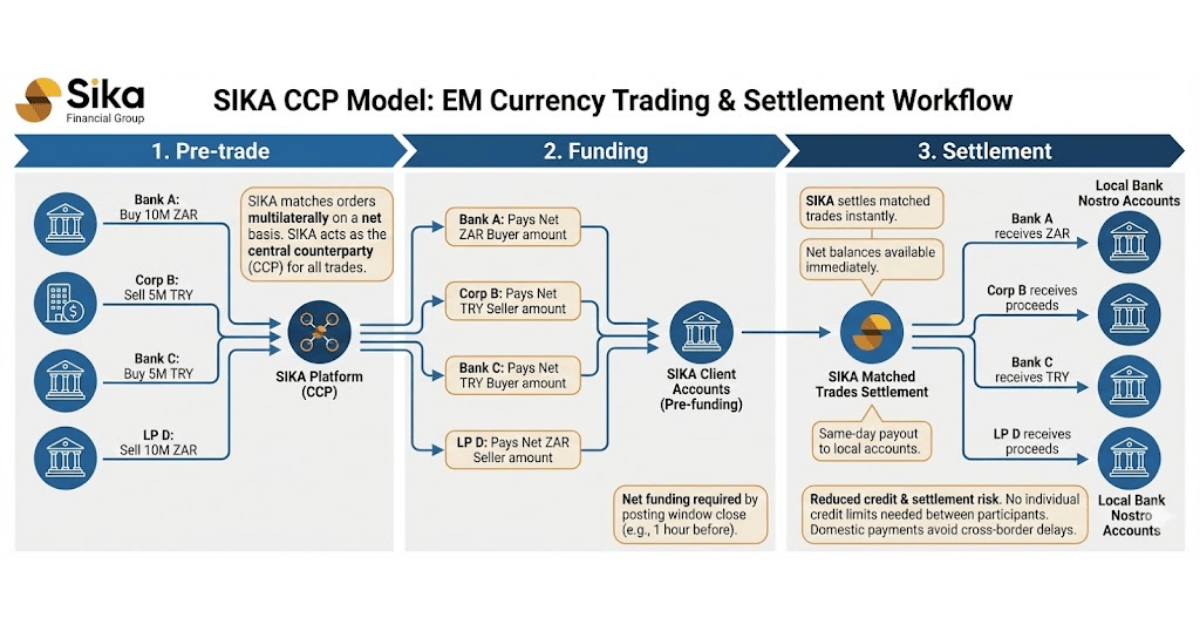

SIKA’s FX Platform: A CCP-Based EM FX Liquidity & Settlement Model

The new offering in the space is from SIKA Financial Group. Based in the US, their offering covers the whole currency liquidity and settlement workflow using a CCP construct.

Their model has three core elements/components:

The Three Core Components of SIKA’s EM FX Platform

1) Pre-trade: Liquidity requests and multilateral matching

Orders (liquidity requests) are submitted to the SIKA platform in two posting windows per day. Supported by liquidity providers, SIKA attempts to match these orders on a multilateral, net basis, increasing the likelihood of fills. SIKA acts as the CCP and stands between all participants. Underlying counterparts are not disclosed to each other and do not need bilateral FX credit lines with every other participant.

2) Funding: Pre-funded net positions

For all orders that can be matched, the net funding requirement must be in place no later than one hour before the posting window closes. Participants pre-fund against their expected activity rather than managing many bilateral pre-funding relationships.

3) Settlement: Instant allocation and same-day recycling

Once all funds are in, matched liquidity requests are settled instantly into SIKA client accounts. Net balances are available immediately. As a rule, client funds are paid out the same day, with overnight balances being the exception. SIKA does not act as a correspondent bank and does not make third-party payments.

The currencies covered by the SIKA platform include both fiat currencies and digital assets, including stablecoins, all managed using the same core process.

Why SIKA’s EM FX Model Matters for Liquidity Management

For many EM FX participants, the constraint today is not just FX liquidity, but the bandwidth to analyse and manage credit risk across a wide range of emerging-market banks, brokers and local institutions. That naturally limits how many EM FX liquidity providers they can sensibly deal with and, by extension, their ability to achieve best execution.

By using a CCP model with pre-funding, SIKA widens the pool of potential liquidity providers and local participants. In some cases, orders from two local players can simply be crossed on the platform, similar to internal or secondary FX trading inside a large bank that sees both sides of the flow.

The centralisation at an exchange and CCP offers significant efficiencies. The safe settlement model today for clients could be described as “ pay, hope and wait”. By hope, I mean hope that the counterpart sees the incoming funds and applies them properly. By wait, I mean sit patiently until those funds are applied and the corresponding payment is initiated. There are lots of ways in which this might drag on or go wrong.

SIKA’s centralised FX order matching and settlement infrastructure aims to remove much of that uncertainty by making the process more predictable and less operationally intensive.

Reducing Liquidity Fragmentation with Posting Windows

In all things liquidity management, having cash scattered across multiple accounts and platforms makes the job harder. Pre-funding is awkward but often unavoidable in EM FX markets.

SIKA’s fixed posting windows help firms manage this pain. Clients pre-fund their SIKA accounts based on expected activity, and as long as funds are in place when the window closes, matched orders are executed and settled. This concentrates liquidity on a single platform and reduces the number of fragmented EM FX pre-funding positions that treasury teams must oversee.

Simplifying Credit Risk: One Counterparty Instead of Many

Under today’s EM FX market structure, an EM counterparty is often asked to pay upfront to trade. Even when that is not required, the counterparty still needs to analyse and manage credit exposure to each liquidity provider they trade with. With limited resources, this usually means working with just one or a handful of providers, reducing competition and pricing transparency.

How SIKA Changes the Credit Risk Calculation

🔹 Single risk assessment: Each participant only needs to assess SIKA, not every other market participant.

🔹 Ring-fenced client funds: Customer balances at SIKA are segregated from the operating company. From a credit perspective, they are treated more like secured receivables than unsecured bank deposits.

🔹 Multilateral market pricing: In a multilateral order book where trades reference mid-rates between bids and offers, participants may see improved execution versus dealing bilaterally with a small set of providers.

Net funding from SIKA’s FX settlement is recycled or returned the same day to clients’ Nostro accounts at local banks. Because these are domestic payments, they avoid the usual delays and friction associated with cross-border transfers.

Where Stablecoins and New Rails Fit In

On existing fiat payment rails, there is no obvious way to earmark a slice of a currency balance for a specific marketplace or FX order, which limits how far settlement risk can be reduced. Projects such as Fnality may change this over time, but today the trade-off remains clear: a platform such as SIKA can simplify processes and potentially improve prices, but participants still need to fund the platform and take some level of credit risk on SIKA.

Stablecoins, particularly in EM markets, are already gaining momentum. Here, the technology exists to avoid both pre-funding and taking credit risk on the entity holding the pre-funds. Earmarking and interoperability are the key enablers.

From Pre-Funding to Atomic Settlement

🔸 With a Web 3.0 wallet, market participants can earmark a specific amount of a stablecoin or digital asset for a particular order on a particular exchange.

🔸 Those funds can only move if the order is executed or cancelled bi-laterally, enabling true atomic netting and settlement for EM FX flows.

🔸 This approach avoids liquidity fragmentation and removes credit exposure to pre-funding intermediaries.

For more on why stablecoins can be superior for payments and settlement, see “Things Stablecoin: They are like Heineken – refreshing the parts other payment rails can’t reach”.

Current Scope and Roadmap

As the SIKA platform stands today, the focus is on spot EM FX flows. Forwards and swaps are not yet available, but they are natural candidates for a future “version 2.0” of the platform as the model evolves and adoption grows.

Conclusion: A Step Forward for EM FX TradinOrder Matching & Settlement

SIKA’s FX platform offers a meaningful improvement on the EM FX status quo. By combining a CCP-based model, multilateral netting and pre-funded settlement within fixed posting windows, it can help reduce settlement risk and delay, simplify credit risk analysis, and expand access to EM FX liquidity.

As stablecoin adoption accelerates and new payment rails mature, there is a clear opportunity to evolve towards true atomic netting and settlement, particularly for EM FX flows. For now, SIKA provides a more efficient, centralised way for participants to access EM FX liquidity and manage settlement risk in a market where these problems have been stubbornly hard to solve.

Found this interesting? Become a member of LiquidityFinder and get daily industry news direct to your inbox — join here.

|

Olaf is a liquidity and financial services expert. He is the founder of 3C Advisory You can message Olaf directly here. |

Why is it so hard to settle Emerging Market FX trades?

Settling EM FX trades is difficult because most EM currencies sit outside CLS and do not benefit from PvP (Payment versus Payment) settlement. Firms often have to pay away funds without certainty that the counterparty will deliver on time, while also dealing with time-zone differences, local banking constraints and weaker payment infrastructure. All of this creates more settlement risk, longer settlement cycles and heavier operational workloads than in G10 FX.

Why are Emerging Market currencies not included in CLS for FX settlement?

CLS coverage is limited to currencies and jurisdictions that meet specific legal, regulatory and infrastructure standards. Many EM currencies do not yet satisfy those requirements, or the local ecosystem has not prioritised CLS participation. As a result, EM FX flows remain largely outside PvP settlement, forcing market participants to rely on bilateral arrangements, pre-funding and manual processes to manage risk.

What are the main settlement risks in Emerging Market FX?

The primary risks are settlement risk (the danger that you pay away funds and the counterparty fails to deliver) and credit risk (the risk that a counterparty defaults while holding your money). These are amplified by delays in local payment systems, misallocation of incoming funds and inconsistent cut-off times. In practice, EM FX traders can be exposed for longer and with less transparency than in well-automated G10 markets.

How does non-CLS FX settlement work for Emerging Market currencies?

Non-CLS EM FX settlement is typically handled bilaterally between counterparties. Payments are sent via correspondent banks or local payment systems, often on a gross or partially netted basis. Without PvP, one party sends funds and then waits for the counterpayment to arrive, monitoring confirmations and reconciliations manually. This “pay and wait” model is operationally intensive and leaves both sides exposed until the full trade has settled.

What is PvP (Payment versus Payment) in FX and why don’t EM currencies have it?

PvP is a settlement mechanism that ensures the two legs of an FX trade are exchanged simultaneously, so neither party can lose the full principal amount if the other defaults. It is delivered in practice through infrastructures such as CLS. Many EM currencies are not part of those infrastructures due to legal, regulatory, volume or infrastructure constraints. Without PvP, EM FX settlement remains sequential and riskier, with one party effectively funding the other until the trade fully completes.

What are the common models for Emerging Market FX settlement (gross, netting, pre-funding)?

EM FX settlement usually follows one of three models:

Gross settlement: each trade settles individually, with full settlement and credit risk between two parties.

Bilateral netting: counterparties net their buys and sells per currency pair and settle a single net amount, reducing payment volumes but not eliminating counterparty risk.

Pre-funding (“safe” settlement): clients pay first and only receive the offsetting leg once funds are received and reconciled, which reduces risk for the liquidity provider but introduces liquidity drag and operational delays for the client.

Why do banks insist on pre-funding for Emerging Market currency trades?

Banks and liquidity providers insist on pre-funding because they are uncomfortable extending unsecured credit in markets that lack PvP and have higher perceived country and counterparty risk. By requiring clients to pay first, they protect themselves against non-delivery and reduce capital exposure. The trade-off is that clients lose flexibility, tie up cash and often face slower, more manual settlement processes.

How does pre-funding fragment liquidity in emerging market FX?

Pre-funding forces clients to spread cash across multiple accounts and providers, often in multiple EM jurisdictions. Each pre-funded balance is ring-fenced for a specific relationship or venue, which makes it harder to deploy liquidity where it is most needed. This fragmentation complicates treasury management, increases internal transfer costs and means clients may trade less than they otherwise would simply because moving money is slow and operationally painful.

What is a CCP model in FX trading and settlement?

A central counterparty (CCP) model places a clearing entity in the middle of every trade, so the CCP becomes the buyer to every seller and the seller to every buyer. In EM FX, a platform like SIKA uses a CCP construct to aggregate orders, perform multilateral netting and concentrate settlement flows. Participants face the CCP rather than a wide network of bilateral counterparties, which simplifies credit risk management and allows funding to be managed on a net, rather than gross, basis.

Can stablecoins reduce credit risk in EM FX settlement?

Stablecoins have the potential to reduce credit risk by allowing funds to be earmarked in a wallet for a specific order on a specific venue. Rather than pre-funding a third party and taking unsecured exposure, a participant can lock a stablecoin balance that only moves if the order is executed or cancelled. This can remove the need to trust an intermediary with free cash balances and can support atomic settlement, where the FX trade and movement of funds happen simultaneously on-chain.

What is the future of Emerging Market FX settlement with stablecoins and new payment rails?

As Web 3.0 infrastructure, stablecoins and new payment rails mature, EM FX settlement is likely to move towards atomic, real-time models with programmable earmarking of funds. CCP-style platforms can combine multilateral netting and credit-risk centralisation with on-chain settlement that only releases funds when trades complete. In this future state, EM FX participants could enjoy better liquidity, lower settlement risk and far less reliance on slow, manual pre-funding relationships.

Share this article

Comments

Most Recent

Find The Right Partners for

Your Trading Business

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Sign Up with LinkedIn

n in-depth review of TMGM (TradeMax Global Markets), the ASIC-regulated ECN broker offering raw spreads from 0.0 pips, MT4 and MT5, copy trading via HUBx and ZuluTrade, and 24/7 multilingual support across four regulated jurisdictions. Find out if TMGM belongs on your shortlist.

LiquidityFinder's Sam Low sits down with Nathan Sage, founder and CEO of Sage Capital Management, to trace his journey from FX fund manager to running a Bitcoin fund doing $1BN a day in 2016 — and how that experience of pain built one of the most connected prime brokerages in the digital assets market today.

Klarna is partnering with Coinbase, raising stablecoin-denominated funding and launching KlarnaUSD. We break down the treasury logic, merchant incentives and agentic AI payments angle — and what other CFOs should take from it.

A comprehensive interactive guide to 50+ global financial regulators - including FCA, ASIC, CFTC, MAS and ESMA - rated across five dimensions: risk management, licence value, investor protection and more. Updated 2026.

Gold at record highs, oil as a meme stock, and crypto exchanges eyeing your clients. Watch our expert panel - Gold-i, Your Bourse, Tapaas and Devexperts - discuss broker risk management, , AI trading and the MetaTrader debate.

Over a long tapas lunch in Shoreditch, London, Sam Low sits down with Peter Brooks and Jess Reed from ADMISI eFX, the dedicated electronic FX desk operating inside one of the world's largest agricultural commodities companies. What emerges is a compelling case for why this largely unknown operation deserves serious attention from brokers, payments firms, corporate treasuries, and digital asset companies alike.

Explore live spread and quote benchmarks powered by the Tradefora Composite Index (TCI), an independent dataset aggregated from multiple FX and CFD brokers. View average, minimum and maximum spreads by instrument and timeframe, plus composite bid/ask quote data updated continuously at millisecond precision.

In Part 6 of his A-Book STP series, Youssef Bouz from GCC Brokers looks at how the rise of algorithmic and AI-assisted trading is forcing brokers to rethink risk models, revenue strategy, and long-term sustainability, and why trader longevity, not short-term extraction, is the real measure of a resilient execution business.

Create Your FREE Account

Get access to latest news, updates, real-time data, brokerage and trading firm insights and customized information feeds.

When traders request withdrawals, the speed and reliability of processing reveals more about your infrastructure than any marketing page ever could. Introduction: I remember sitting with a broker who…

Yields pressing 2026 highs, the Fed leaning hawkish, and gold's triangle threatening to break — here's what's on the calendar this week.

Explore the risks of copy trading, assess if it's safe, and learn if copy trading works. Discover professional risk management strategies to protect your investments.... Read more on tradecopier.o…

Market drivers and catalysts Equities: US equities rose, Europe paused near highs, and Asia’s chip-heavy markets rallied as AI optimism broadened. Fixed Income: US long treasury yields ease lower, Sho…

Markets keep climbing as if nothing can go wrong. While oil prices remain volatile, global yields surge, economic data weakens and recession risks build beneath the surface, investors are once again c…

Your Bourse will be exhibiting as a Gold Sponsor at the Online Trading Expo Hong Kong 2026, taking place May 27 and 28 at AsiaWorld-Expo. The expo is one of the primary industry gatherings for brokers…

Yes, people have used AI trading bots and some have made money, but it’s not as simple as “turn on and earn profit.” AI trading bots are automated systems that analyze market data and execute trades b…

Discover how news filters in forex trading help avoid high-impact events, protect trades, and enhance strategies with trade copiers. Learn to stop copy trading during volatile news.... Read more on tr…

Binance has launched Pre-IPO perpetual futures contracts, providing early market exposure to high-profile private companies like SpaceX, democratising access to pre-public listing trading opportunities for eligible users.

Cantor, a global investment bank, has received approval from the Financial Services Regulatory Authority (FSRA) of ADGM to conduct regulated financial activities in Abu Dhabi, marking a significant expansion in the Middle East.

Curious about the latest Bitcoin price action? Discover if BTC/USD will keep dropping using daily chart analysis and a proven crypto trading strategy.

Empire FX has appointed Sahil Patel as Chief Operating Officer to lead its global operations and accelerate expansion across Africa, the Middle East, and Asia. Patel brings extensive experience from Pepperstone and IG Group to strengthen infrastructure and enhance client experience.

WTI dropped below $100 after reports suggested a US-Iran agreement could be getting closer, with Arab media outlet Al Hadath reporting that Pakistan’s army chief Asim Munir may visit Iran to announce…

Sui has announced gasless stablecoin transfers, a new protocol-level feature enabling users and businesses to send supported stablecoins without gas fees. Fireblocks has already integrated the solution, marking a significant step towards simplifying digital asset payments for institutional and retail users.

Discover what reverse copy trading is, explore social trader tools and copy trading platforms for online trade copying. Optimize your strategy with professional insights on reverse trading techniques.…

NVDA enters tonight's $5.7T print with a stacked deck against it — the bear case needs only one leg to break, the bull case needs all three to clear elevated whispers.

dxFeed has integrated Kalshi, a CFTC-regulated prediction market exchange, into its Event-Based Contracts Market Data Feed, offering real-time data on binary outcome markets.

MEXC reports a sharp increase in traditional finance futures trading, with AI semiconductor assets leading the surge. The platform highlights how crypto exchanges are becoming a preferred route for users to gain exposure to TradFi markets, offering zero fees and stablecoin settlement.

Bitget Wallet has integrated xStocks, expanding its tokenised equities and RWA offering to over 300 assets for its 90 million users. The move provides self-custodial access to tokenised stocks, ETFs, and commodities, alongside cryptocurrencies, with low fees and gasless execution.

MARKET REPORT UK jobs data adds to GBP uncertainty ahead of tomorrow's CPI To talk to us about your next trade, call 020 7778 7500 or hit the button below Email us USD falls for the first time…

Feed